47

Innovative waste management products European market survey Technology Review 147/2003 Christoph Genter

Innovativewaste management productsEuropean market survey

Technology Review 147/2003

Christoph Genter

Tekes• Innovative w

aste managem

ent prod

ucts – Europ

ean market survey

Technology Review

147

03

November 2003 ISSN 1239-758XISBN 952-457-139-0

National Technology AgencyKyllikinportti 2

P.O. Box 69, FIN-00101 Helsinki, FinlandTel. +358 105 2151, fax +358 9 694 9196

e-mail: [email protected]

Innovative waste management products – European market surveyTechnology Review 147/2003

For more information, please contact

Arto SilvennoinenTel. +358 15 535 5088

Helena ManninenTel. + 358 010 521 5888

Innovativewaste management products

European market survey

Christoph Genter

National Technology Agency

Technology Review 147/2003Helsinki 2003

Tekes – your contact for Finnish technology

Tekes, the National Technology Agency, is the main financing organisationfor applied and industrial R&D in Finland. Funding is granted from the statebudget.

Tekes’ primary objective is to promote the competitiveness of Finnish indus-try and the service sector by technological means. Activities are aimed at di-versifying production structures, increasing productivity and exports andcreating a foundation for employment and social well-being. Tekes financesapplied and industrial R&D in Finland to the extent of nearly 400 million eurosannually. The Tekes network in Finland and overseas offers excellent chan-nels for cooperation with Finnish companies, universities and research insti-tutes.

Technology programmes – part of the innovation chain

The technology programmes are an essential part of the Finnish innovationsystem. These programmes have proved to be an effective form of coopera-tion and networking for companies and the research sector for developinginnovative products and processes. Technology programmes promote de-velopment in specific sectors of technology or industry, and the results ofthe research work are passed on to business systematically. The pro-grammes also serve as excellent frameworks for international R&D coopera-tion. Currently, 35 extensive technology programmes are under way.

Copyright Tekes 2003. All rights reserved.

This publication includes materials protected under copyright law, thecopyright for which is held by Tekes or a third party. The materials appearingin publications may not be used for commercial purposes. The contents ofpublications are the opinion of the writers and do not represent the officialposition of Tekes. Tekes bears no responsibility for any possible damages

arising from their use. The original source must be mentioned when quotingfrom the materials.

ISSN 1239-758XISBN 952-457-139-0

Cover: Oddball GraphicsPage layot: DTPage Oy

Printers: Paino-Center Oy, 2003

Preface

The Streams Technology Programme (2001–2004) – Recycling Technologies and Waste Manage-ment – focuses on developing products and services for waste management and the recycling andreuse of waste materials. New, more advanced technology will be needed in order to fulfil the newand more stringent stipulations for waste management, recycling and reuse which now apply to theentire EU. Finnish industrial companies operating in the environmental sector could benefit fromdrawing on information and communications technology (ICT) and biotechnology in their tradi-tional waste management products. Consequently, the development of intelligent products forwaste management and reuse has been made one of the main objectives of the Streams TechnologyProgramme.

This report was commissioned by the Tekes Streams Technology Programme and written duringthe summer of 2003. The purpose of the report was to give an overview of the market potential ofFinnish intelligent waste management products within the European Union. The report was pro-duced by AMCG Unternehmensberatung GmbH International Management Consultants. Thework was supervised and monitored by the Streams Technology Programme management group.The members of the group were Juha Kaila, YTV (the Helsinki Metropolitan Area Council); AimoAalto, the Ministry of Trade and Industry; Osmo Bolander, Lassila&Tikanoja Plc; Keijo Hämä-läinen, Efirec Oy; Juhani Ilmola, SOK Corporation; Kari Kangas, Tanacorp Oy Ltd; Markku Salo,the Finnish Solid Waste Association; Matti Vehkalahti, the Ministry of the Environment; ArtoSilvennoinen, Consulting Engineers Paavo Ristola Ltd; Helena Manninen, Tekes and AskoVesanto, Tekes.

The report is intended for use by Finnish corporations in the waste management sector and for com-panies which may be able to adapt and develop their existing products for use in the waste manage-ment sector. The report gives an overview of the present situation in the waste management sectortogether with business opportunities in Europe.

Tekes wishes to express its warmest thanks to Christoph Genter and his team at AMCG GmbH.The management group of the Streams Technology Programme also deserves gratitude for creativeand constructive work supervision.

Helsinki, October 2003

Tekes – The National Technology Agency of Finland

Contact information

AMCG Unternehmensberatung GmbHInternational Management ConsultantsLandshuter Allee 45D-80637 Munich, GermanyPhone +49-89-130 757 0

Contact person

Christoph Genter, e-mail: [email protected]

Contents

Foreword

1 Objectives and content of the study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Methodology and timing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

3 Waste management business in Europe – overview . . . . . . . . . . . . . . . . . . . . . . . . 5

4 Markets for intelligent waste management products and services – overview. . 13

5 Characterization of intelligent products and services . . . . . . . . . . . . . . . . . . . . . . 175.1 Waste prevention . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

5.2 Waste collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 185.2.1 New collection trucks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 185.2.2 Separation of collection and transport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205.2.3 Route planning and supervision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 225.2.4 Individual billing systems. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245.2.5 Deposit automats for bottles/cans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 265.2.6 Suction systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

5.3 Waste handling. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 295.3.1 Automated sorting plants . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 295.3.2 Electronic scrap handling and recycling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

5.4 Waste recycling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 335.4.1 Mechanical biological treatment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 335.4.2 Optimization of grate incinerators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 365.4.3 New incineration technologies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

6 Attractive businesses for the Finnish waste industry . . . . . . . . . . . . . . . . . . . . . . 39

Tekes Technology Reviews. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

1 Objectives and content of the study

The objective of this study is to identify attractive busi-nesses for the Finnish waste industry in the area of intelli-gent waste management products and services.The follow-ing topics are covered in detail by the study:

• The waste management service business in Europe

– an overview of the current business and its mainactors in Europe

• Current and future markets for intelligent waste manage-ment products and services

– including identification of these products/servicesand evaluation of the technologies, markets andsuppliers

• Selection of attractive businesses for the Finnish wasteindustry

– the selection is based on the competitiveness of theFinnish waste industry and on the attractiveness ofthe different businesses for intelligent products andservices.

Tekes has contracted AMCG to perform the analysis. Thestudy was conducted for the Finnish environmental indus-try as well as for other Finnish industries offering the re-quired products and services. The results should serveFinnish companies as a basis for the development of prod-uct and market strategies to allow them to enter these mar-kets for intelligent products and services in Europe.

The study examines intelligent waste management prod-ucts and services which are used for the prevention andtreatment of municipal solid waste (MSW). The goal of thestudy was to analyze the market volume and future potentialof these products within the European Union, i.e. in the cur-rent 15 EU member states as well as in the 10 new EU mem-ber states (as from 2004). Intelligent waste managementproducts and services are not a defined group of productsand/or services. In the course of this study, “intelligent prod-ucts/services” means

• innovative concepts for waste prevention or wastetreatment,

• consisting of one or many different products and/orservices,

• creating benefits for the customer in terms of costs,quality, etc.

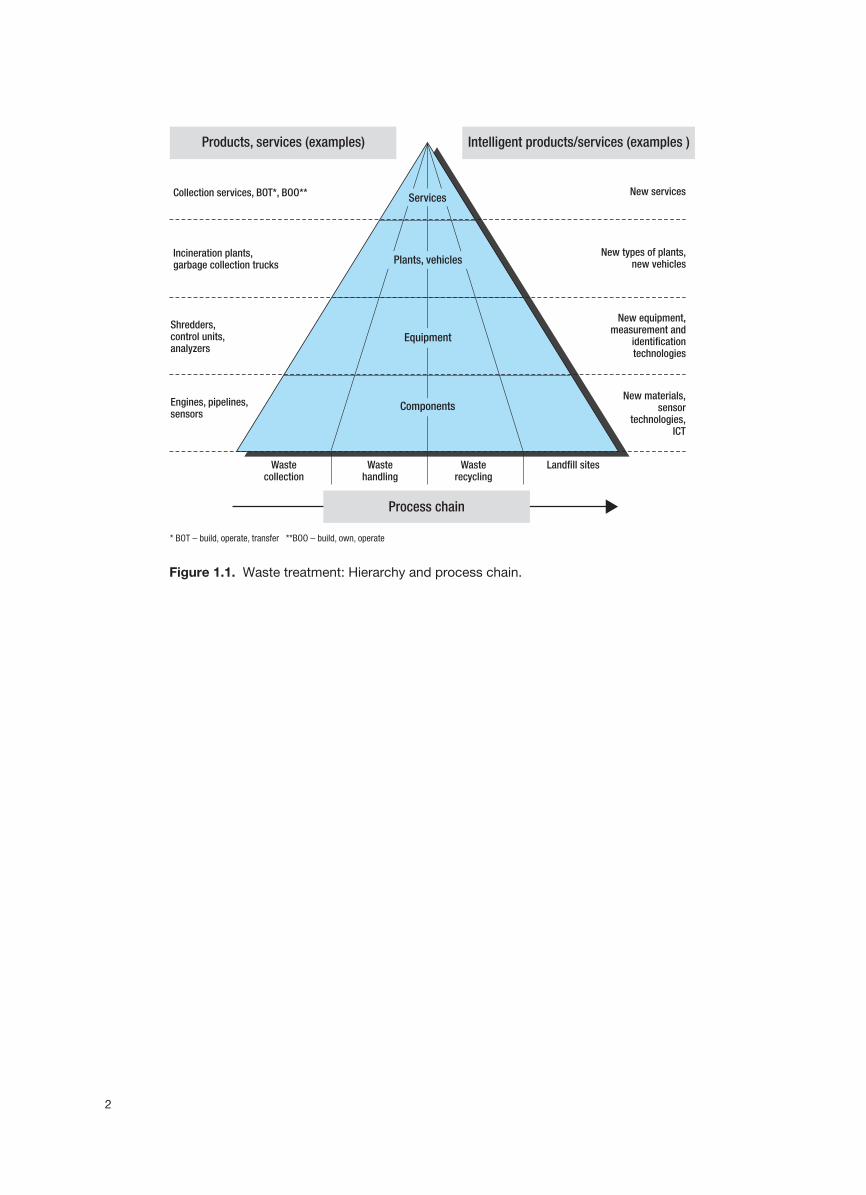

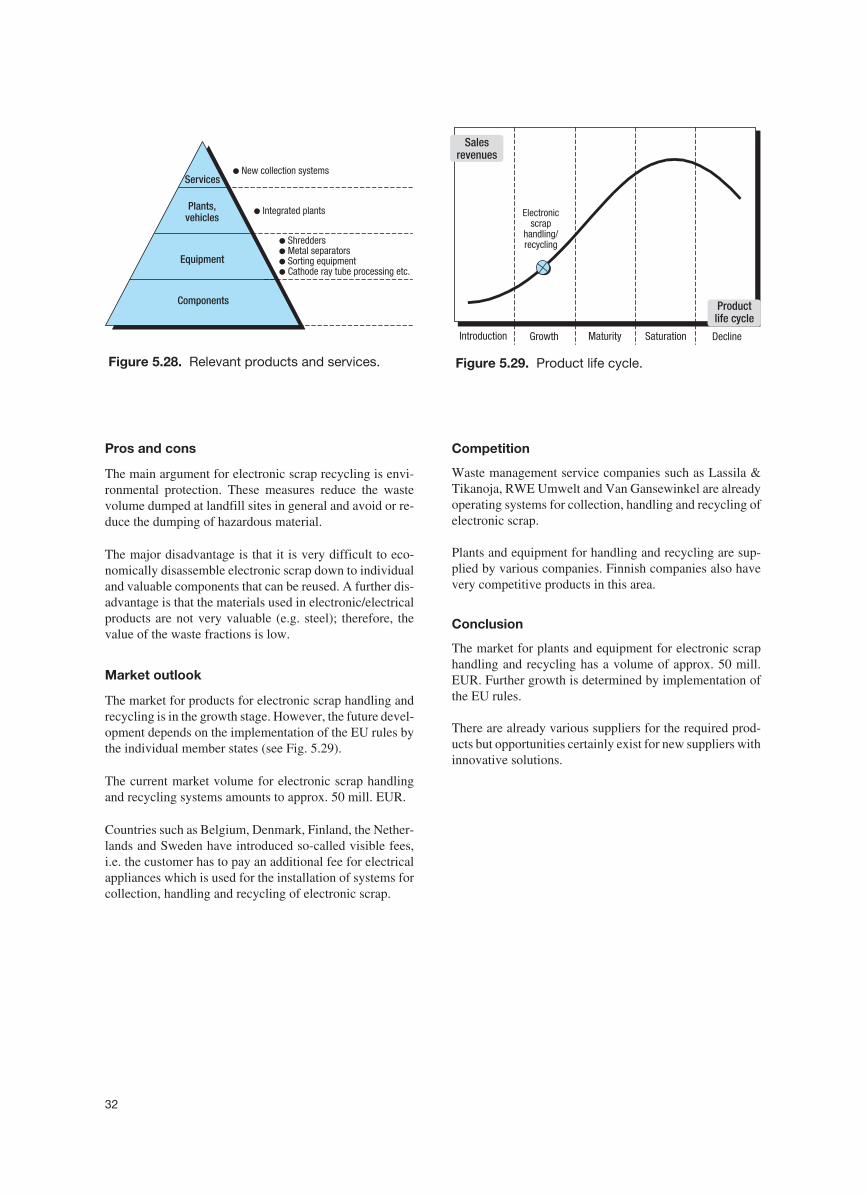

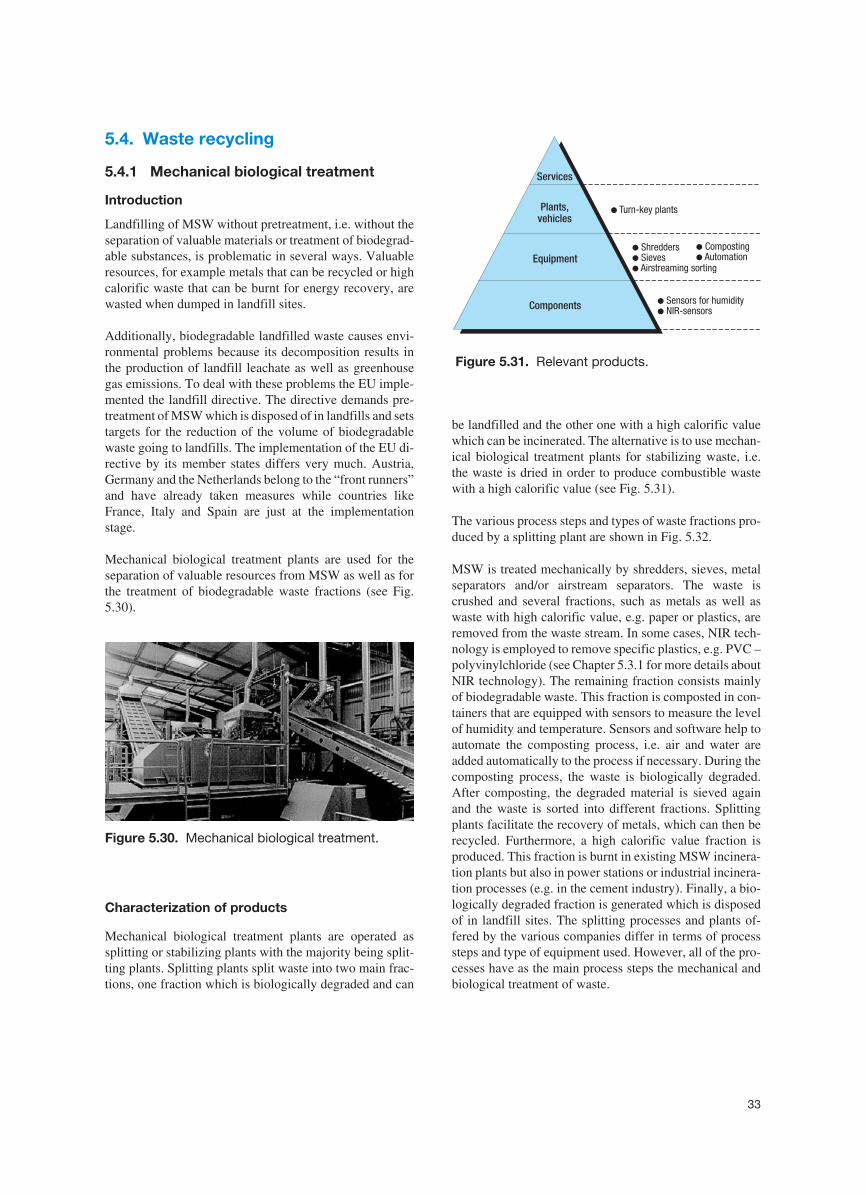

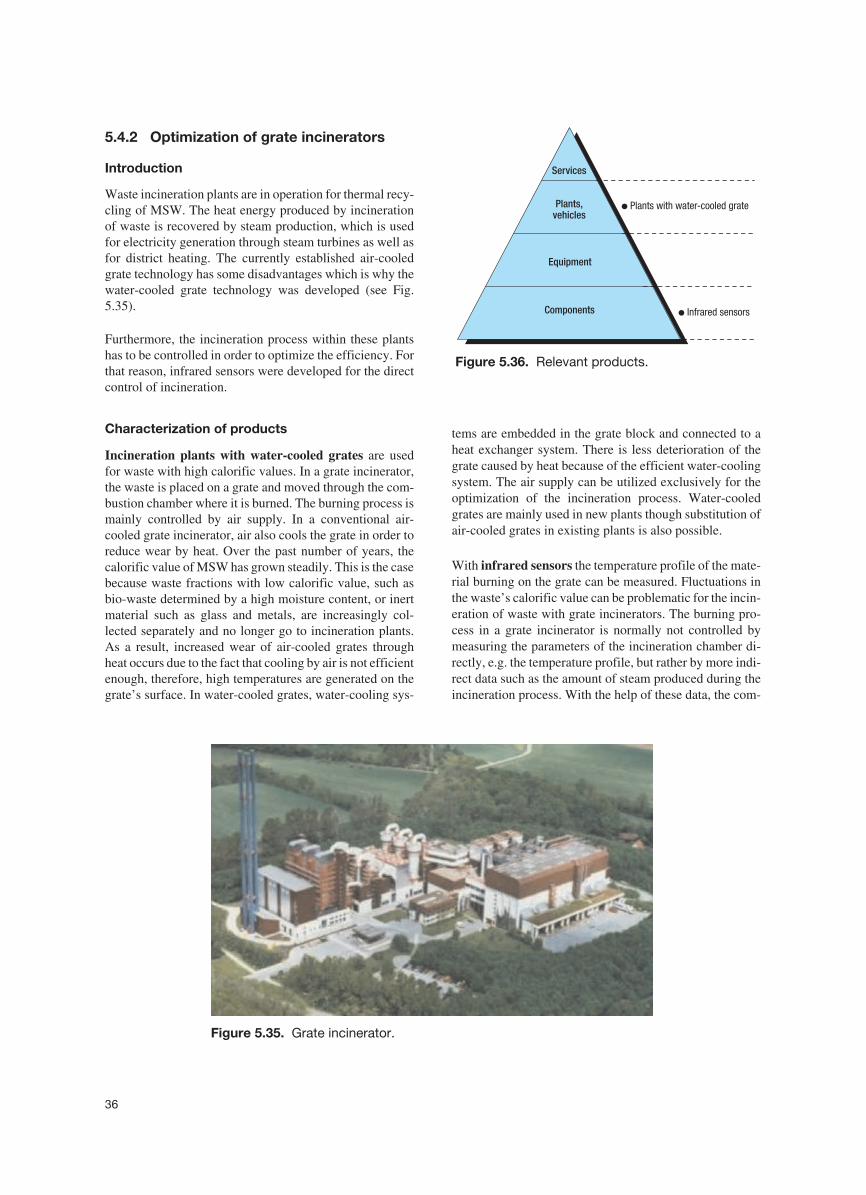

Intelligent products and services are developed for wasteprevention or waste treatment. The process chain for wastetreatment covers waste collection, waste handling, wasterecycling and disposal (landfill sites). Intelligent productscan be used for all steps of the process chain. Furthermore,the hierarchy of waste treatment solutions can be structuredtop- down into services, plants/vehicles, equipment andcomponents. Figure 1.1 demonstrates the waste treatmentprocess chain and hierarchy as well as examples of intelli-gent products and services.

1

2

Collection services, BOT*, BOO**

Incineration plants,garbage collection trucks

Engines, pipelines,sensors

Shredders,control units,analyzers

Products, services (examples)

New services

New types of plants,new vehicles

New materials,sensor

technologies,ICT

New equipment,measurement and

identificationtechnologies

Intelligent products/services (examples )

Wastecollection

Wastehandling

Wasterecycling

Landfill sites

Process chain

* BOT – build, operate, transfer **BOO – build, own, operate

Components

Equipment

Plants, vehicles

Services

Figure 1.1. Waste treatment: Hierarchy and process chain.

2 Methodology and timing

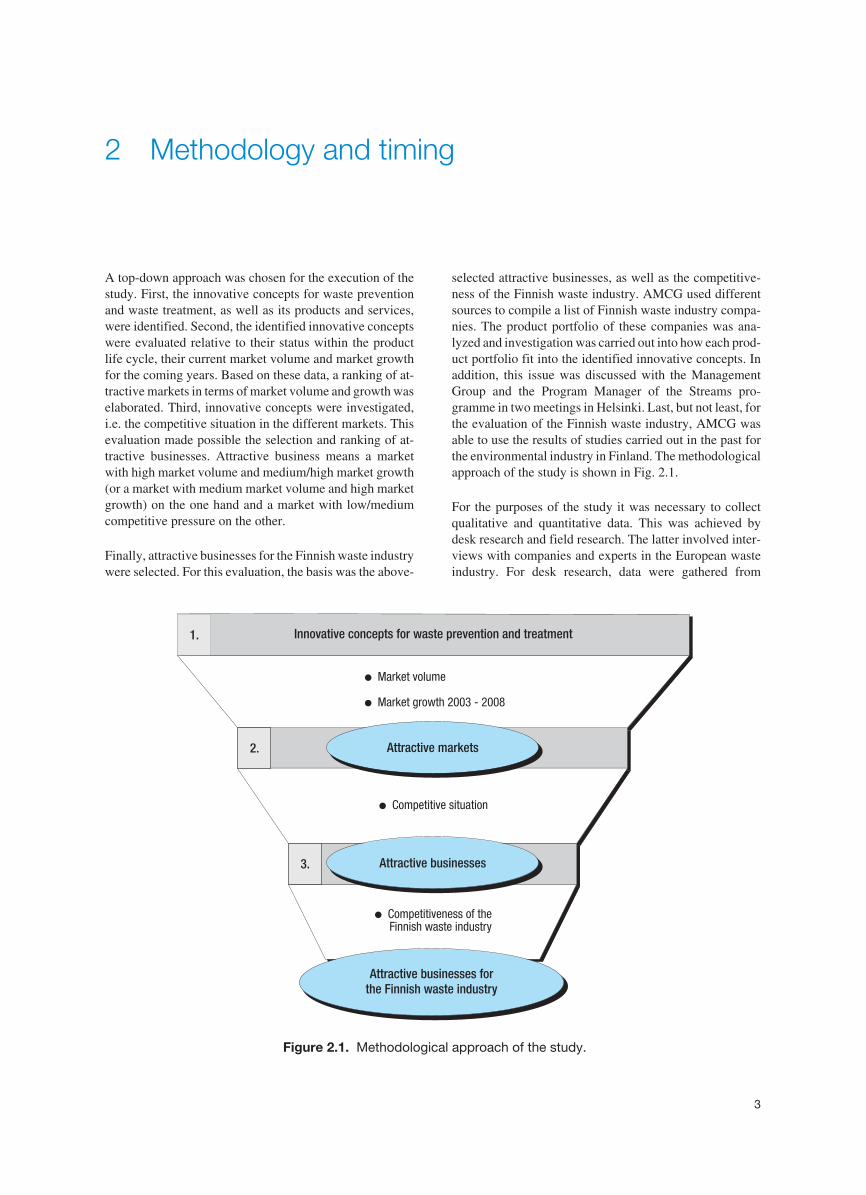

A top-down approach was chosen for the execution of thestudy. First, the innovative concepts for waste preventionand waste treatment, as well as its products and services,were identified. Second, the identified innovative conceptswere evaluated relative to their status within the productlife cycle, their current market volume and market growthfor the coming years. Based on these data, a ranking of at-tractive markets in terms of market volume and growth waselaborated. Third, innovative concepts were investigated,i.e. the competitive situation in the different markets. Thisevaluation made possible the selection and ranking of at-tractive businesses. Attractive business means a marketwith high market volume and medium/high market growth(or a market with medium market volume and high marketgrowth) on the one hand and a market with low/mediumcompetitive pressure on the other.

Finally, attractive businesses for the Finnish waste industrywere selected. For this evaluation, the basis was the above-

selected attractive businesses, as well as the competitive-ness of the Finnish waste industry. AMCG used differentsources to compile a list of Finnish waste industry compa-nies. The product portfolio of these companies was ana-lyzed and investigation was carried out into how each prod-uct portfolio fit into the identified innovative concepts. Inaddition, this issue was discussed with the ManagementGroup and the Program Manager of the Streams pro-gramme in two meetings in Helsinki. Last, but not least, forthe evaluation of the Finnish waste industry, AMCG wasable to use the results of studies carried out in the past forthe environmental industry in Finland. The methodologicalapproach of the study is shown in Fig. 2.1.

For the purposes of the study it was necessary to collectqualitative and quantitative data. This was achieved bydesk research and field research. The latter involved inter-views with companies and experts in the European wasteindustry. For desk research, data were gathered from

3

Innovative and treatmentconcepts for waste prevention

●

●

Market volume

Market growth 2003 - 2008

● Competitive situation

1.

2.

3.

● Competitiveness of theFinnish waste industry

Attractive businesses forthe Finnish waste industry

Attractive businesses

Attractive markets

Figure 2.1. Methodological approach of the study.

sources such as statistics, waste magazines, product bro-chures, annual reports of waste industry companies and da-tabases. In addition, AMCG used the results and experi-ence from numerous studies that were carried out in thepast for the European environmental industry.

The majority of the data were collected through interviewswith companies and experts. AMCG conducted in total 65interviews in Europe. For the identification and evaluationof innovative concepts this issue was discussed with• 23 of the 30 leading waste management service compa-

nies in Europe• 8 public and private organizations of the European waste

industry.

The waste management service companies are the majorusers and clients for waste management products and ser-vices, and also for innovative concepts. Therefore, the fol-lowing topics were discussed with these companies:• What are the main problems with currently used prod-

ucts and services in terms of quality and costs?• Which types of innovative concepts will be used and/or

would be necessary in the future?• What are the main investments the companies will

makein subsequent years?

Furthermore, interviews were conducted with public andprivate organizations in Europe to identify innovative con-cepts; these included Ministries for Environment, environ-mental protection agencies, associations for waste, glass,and plastic recycling and research organizations for envi-ronmental technologies.

The second round of interviews was conducted with com-panies who offer or use the identified innovative concepts.In total, interviews were held with 33 companies in order toevaluate the market and competitive situation for theseconcepts.

The data collected by desk and field research were sub-jected to a plausibility check and finally the required resultswere elaborated according to the methodology describedabove. The study was performed from May to August 2003in close cooperation with the Management Group and theProgram Manager of the Streams programme. The kick-offmeeting for the study took place in mid-May in Helsinki.The interim results were presented and discussed inmid-June and the final results were presented and dis-cussed at the end of August in Helsinki.

4

3 Waste management business in Europe– overview

This chapter covers an overview of the waste managementbusiness in Europe. The value chain for waste manage-ment, waste quantities and waste treatment technologies,market volume for waste management products and ser-vices, major players as well as trends in the industry are de-scribed.

Value chain for waste management

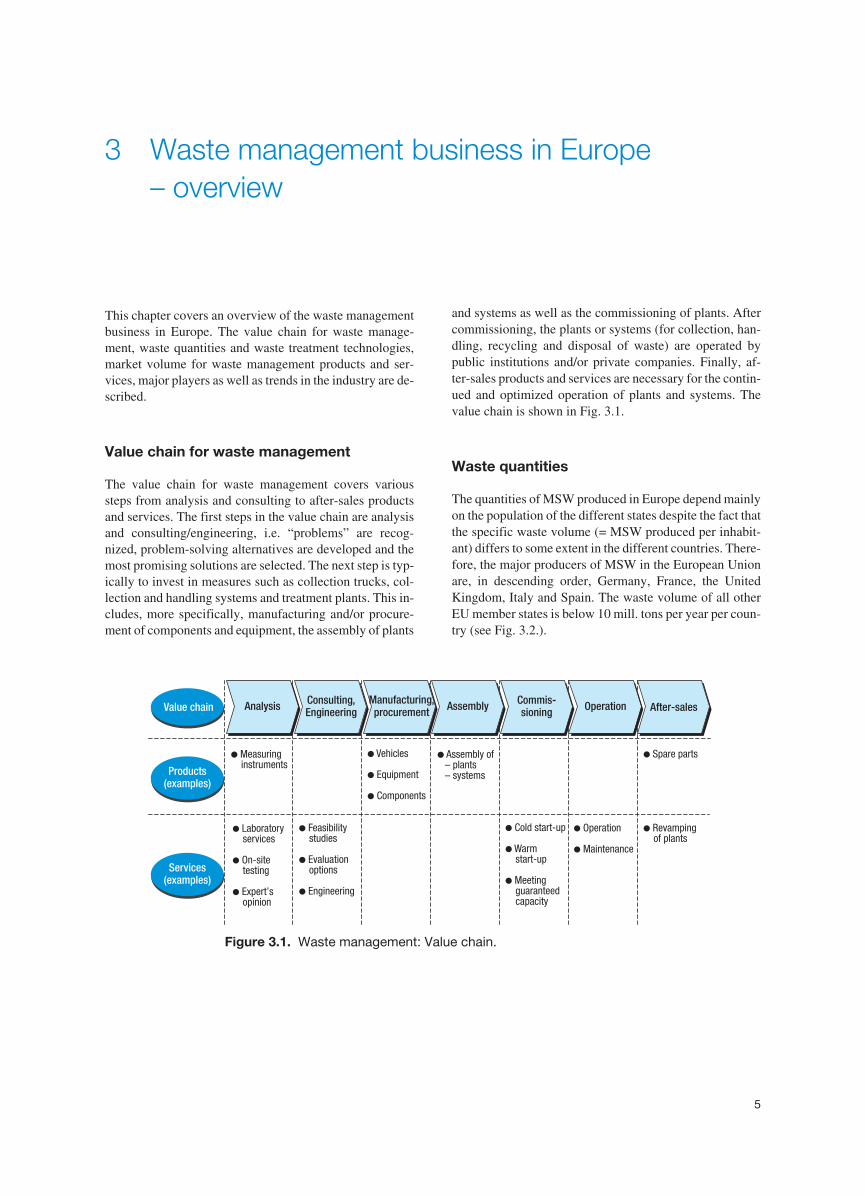

The value chain for waste management covers varioussteps from analysis and consulting to after-sales productsand services. The first steps in the value chain are analysisand consulting/engineering, i.e. “problems” are recog-nized, problem-solving alternatives are developed and themost promising solutions are selected. The next step is typ-ically to invest in measures such as collection trucks, col-lection and handling systems and treatment plants. This in-cludes, more specifically, manufacturing and/or procure-ment of components and equipment, the assembly of plants

and systems as well as the commissioning of plants. Aftercommissioning, the plants or systems (for collection, han-dling, recycling and disposal of waste) are operated bypublic institutions and/or private companies. Finally, af-ter-sales products and services are necessary for the contin-ued and optimized operation of plants and systems. Thevalue chain is shown in Fig. 3.1.

Waste quantities

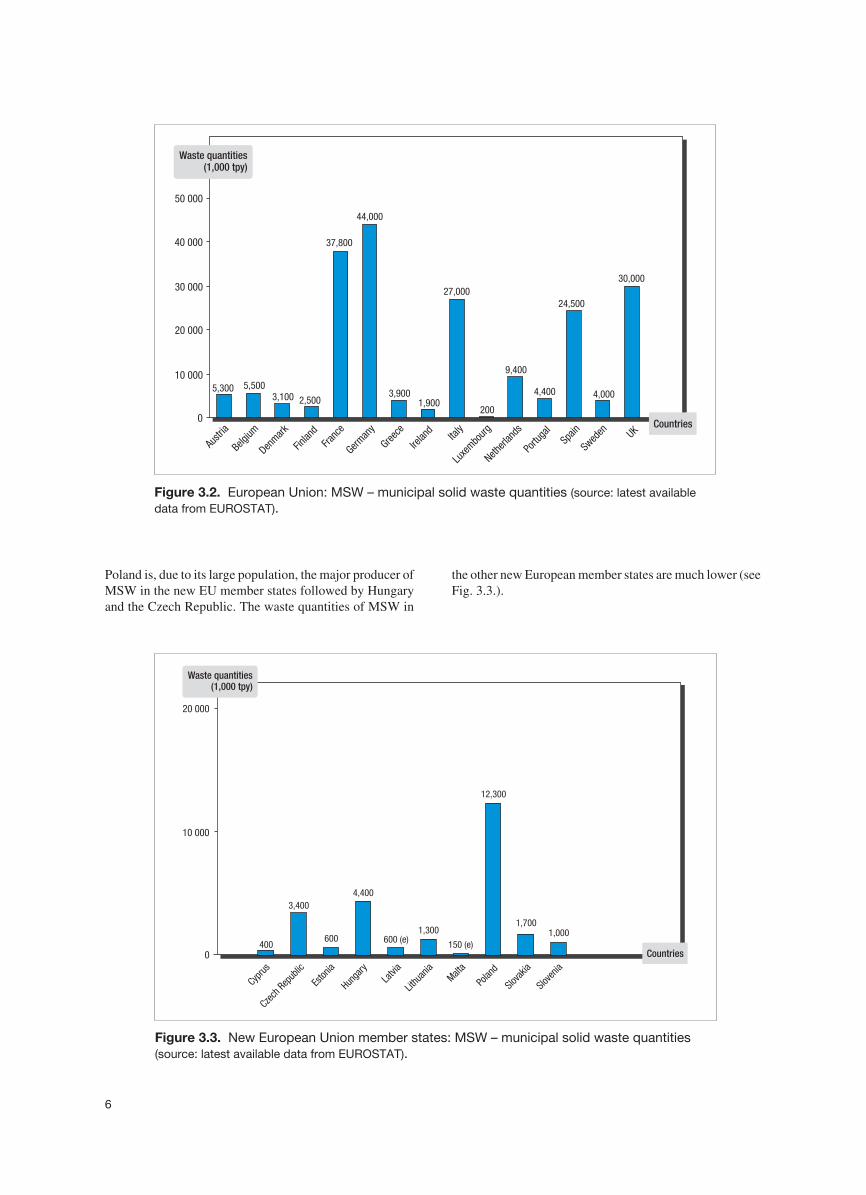

The quantities of MSW produced in Europe depend mainlyon the population of the different states despite the fact thatthe specific waste volume (= MSW produced per inhabit-ant) differs to some extent in the different countries. There-fore, the major producers of MSW in the European Unionare, in descending order, Germany, France, the UnitedKingdom, Italy and Spain. The waste volume of all otherEU member states is below 10 mill. tons per year per coun-try (see Fig. 3.2.).

5

Value chainManufacturing,procurementAnalysis Consulting,

Engineering Assembly Commis-sioning Operation After-sales

● Measuringinstruments

●

●

●

quipment

Components

Vehicles

E

● of– plants– systems

Assembly ● partsSpare

Products(examples)

●

●

●

Laboratoryservices

On-sitetesting

Expert’sopinion

●

●

●

studies

Evaluationoptions

Engineering

Feasibility ●

●

●

Cold start-up

Warmstart-up

Meetingguaranteedcapacity

●

● Maintenance

Operation

Services(examples)

●

plantsRevampingof

Figure 3.1. Waste management: Value chain.

Poland is, due to its large population, the major producer ofMSW in the new EU member states followed by Hungaryand the Czech Republic. The waste quantities of MSW in

the other new European member states are much lower (seeFig. 3.3.).

6

Countries

5,300

Austr

ia

Belgium

Denmark

Finlan

dFra

nce

German

y

Greece

Irelan

dIta

ly

Luxe

mbourg

Netherl

ands

Portu

gal

Spain

Swed

en UK

5,5003,100 2,500

37,800

44,000

3,9001,900

27,000

200

9,400

4,400

24,500

4,000

30,000

0

10 000

20 000

30 000

40 000

50 000

Waste quantities(1,000 tpy)

Figure 3.2. European Union: MSW – municipal solid waste quantities (source: latest availabledata from EUROSTAT).

400 600 (e) 150 (e)

3,400

600

4,400

1,300 1,0001,700

12,300

0

10 000

20 000

Slova

kia

Polan

dMalt

a

Lithu

ania

Latvi

a

Hunga

ry

Eston

ia

Czech

Repub

lic

Cyprus

Slove

niaCountries

Waste quantities(1,000 tpy)

Figure 3.3. New European Union member states: MSW – municipal solid waste quantities(source: latest available data from EUROSTAT).

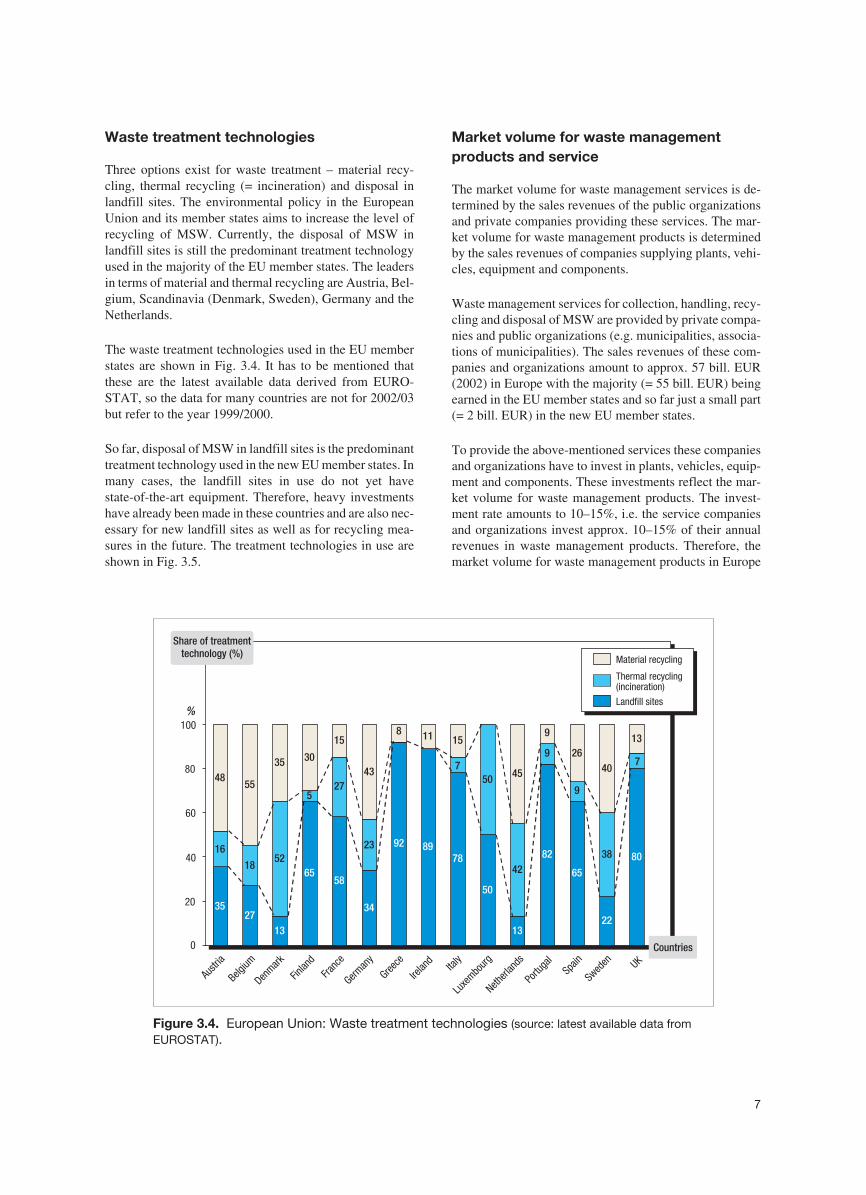

Waste treatment technologies

Three options exist for waste treatment – material recy-cling, thermal recycling (= incineration) and disposal inlandfill sites. The environmental policy in the EuropeanUnion and its member states aims to increase the level ofrecycling of MSW. Currently, the disposal of MSW inlandfill sites is still the predominant treatment technologyused in the majority of the EU member states. The leadersin terms of material and thermal recycling are Austria, Bel-gium, Scandinavia (Denmark, Sweden), Germany and theNetherlands.

The waste treatment technologies used in the EU memberstates are shown in Fig. 3.4. It has to be mentioned thatthese are the latest available data derived from EURO-STAT, so the data for many countries are not for 2002/03but refer to the year 1999/2000.

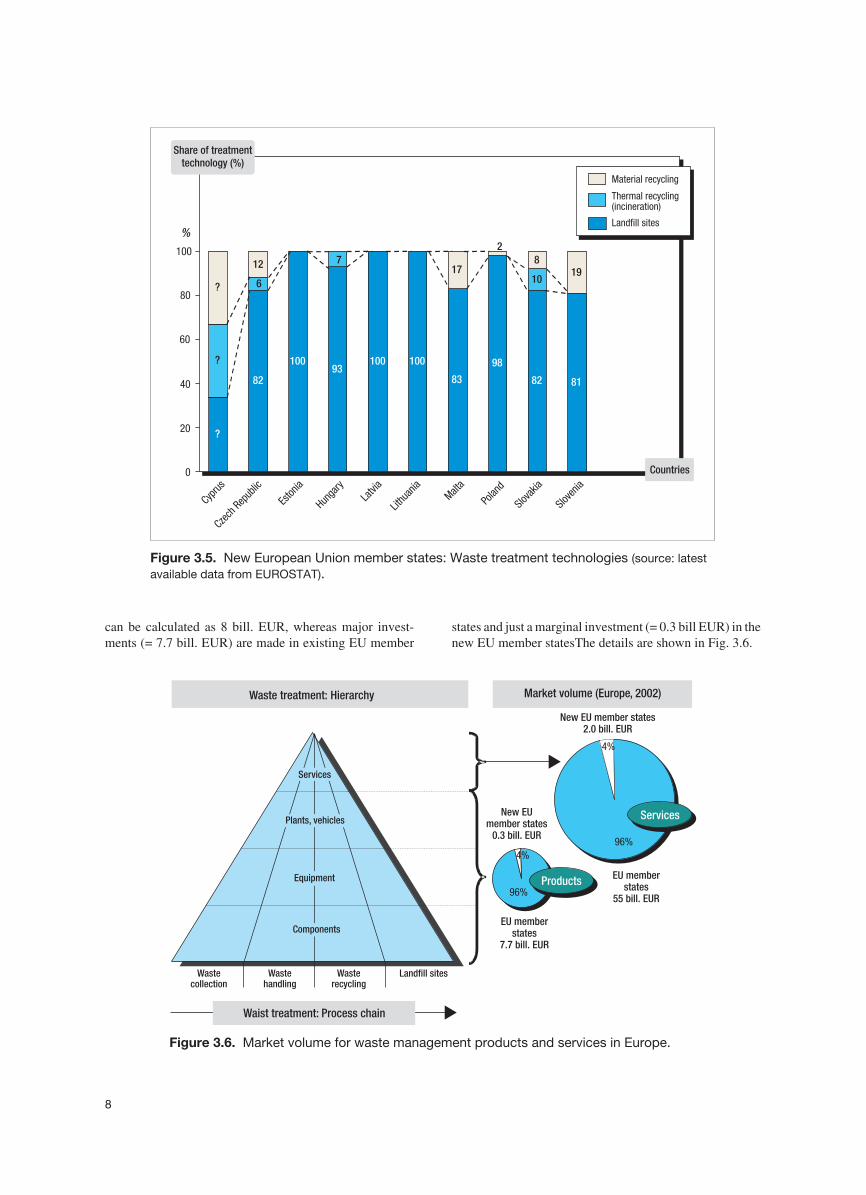

So far, disposal of MSW in landfill sites is the predominanttreatment technology used in the new EU member states. Inmany cases, the landfill sites in use do not yet havestate-of-the-art equipment. Therefore, heavy investmentshave already been made in these countries and are also nec-essary for new landfill sites as well as for recycling mea-sures in the future. The treatment technologies in use areshown in Fig. 3.5.

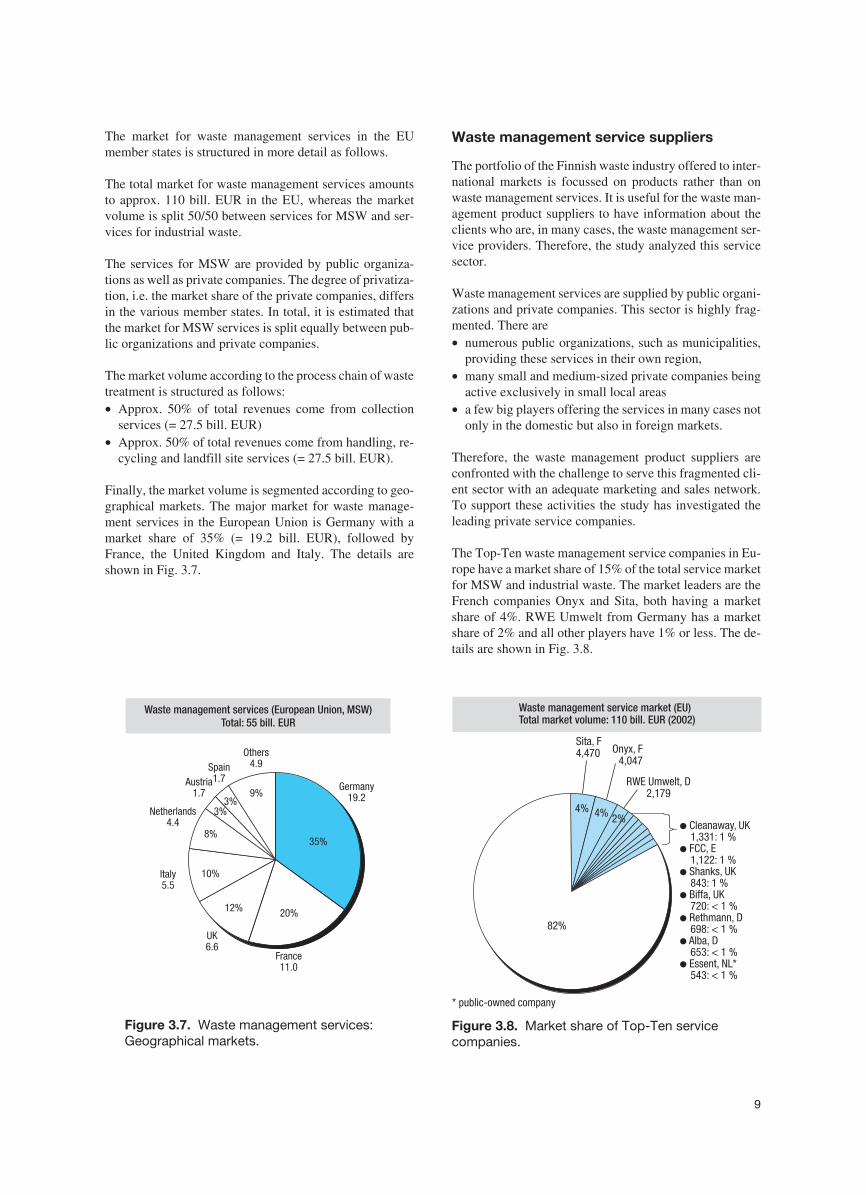

Market volume for waste managementproducts and service

The market volume for waste management services is de-termined by the sales revenues of the public organizationsand private companies providing these services. The mar-ket volume for waste management products is determinedby the sales revenues of companies supplying plants, vehi-cles, equipment and components.

Waste management services for collection, handling, recy-cling and disposal of MSW are provided by private compa-nies and public organizations (e.g. municipalities, associa-tions of municipalities). The sales revenues of these com-panies and organizations amount to approx. 57 bill. EUR(2002) in Europe with the majority (= 55 bill. EUR) beingearned in the EU member states and so far just a small part(= 2 bill. EUR) in the new EU member states.

To provide the above-mentioned services these companiesand organizations have to invest in plants, vehicles, equip-ment and components. These investments reflect the mar-ket volume for waste management products. The invest-ment rate amounts to 10–15%, i.e. the service companiesand organizations invest approx. 10–15% of their annualrevenues in waste management products. Therefore, themarket volume for waste management products in Europe

7

Material recycling

Thermal recycling(incineration)

Landfill sites

Share of treatmenttechnology (%)

3527

13

6558

34

92 8978

50

13

82

65

22

8016

1852

27

23

50

42

9

9

38

4855

35

15

43

8 11 15

45

9

2640

13

7 7

5

30

0

20

40

60

80

100

Countries

%

Austr

ia

Belgium

Denmark

Finlan

dFra

nce

German

y

Greece

Irelan

dIta

ly

Luxe

mbourg

Netherl

ands

Portu

gal

Spain

Swed

en UK

Figure 3.4. European Union: Waste treatment technologies (source: latest available data fromEUROSTAT).

can be calculated as 8 bill. EUR, whereas major invest-ments (= 7.7 bill. EUR) are made in existing EU member

states and just a marginal investment (= 0.3 bill EUR) in thenew EU member statesThe details are shown in Fig. 3.6.

8

Czech

Repub

lic

10093

100

82 81

1019

?

100 98

82 83

?

7

6?

812 17

2

0

20

40

60

80

100

Material recycling

Thermal recycling(incineration)

Landfill sites

Countries

%

Share of treatmenttechnology (%)

Slova

kia

Polan

dMalt

a

Lithu

ania

Latvi

a

Hunga

ry

Eston

ia

Cyprus

Slove

nia

Figure 3.5. New European Union member states: Waste treatment technologies (source: latestavailable data from EUROSTAT).

96%

4%

96%

4%

96%

4%

96%

4%

Waste treatment: Hierarchy Market volume (Europe, 2002)

New EU member states2.0 bill. EUR

New EUmember states

0.3 bill. EUR

EU memberstates

55 bill. EUR

EU memberstates

7.7 bill. EUR

ProductsProducts

ServicesServices

Equipment

Plants, vehicles

Services

Components

Wastecollection

Wastehandling

Wasterecycling

Landfill sites

Waist treatment: Process chain

Figure 3.6. Market volume for waste management products and services in Europe.

The market for waste management services in the EUmember states is structured in more detail as follows.

The total market for waste management services amountsto approx. 110 bill. EUR in the EU, whereas the marketvolume is split 50/50 between services for MSW and ser-vices for industrial waste.

The services for MSW are provided by public organiza-tions as well as private companies. The degree of privatiza-tion, i.e. the market share of the private companies, differsin the various member states. In total, it is estimated thatthe market for MSW services is split equally between pub-lic organizations and private companies.

The market volume according to the process chain of wastetreatment is structured as follows:• Approx. 50% of total revenues come from collection

services (= 27.5 bill. EUR)• Approx. 50% of total revenues come from handling, re-

cycling and landfill site services (= 27.5 bill. EUR).

Finally, the market volume is segmented according to geo-graphical markets. The major market for waste manage-ment services in the European Union is Germany with amarket share of 35% (= 19.2 bill. EUR), followed byFrance, the United Kingdom and Italy. The details areshown in Fig. 3.7.

Waste management service suppliers

The portfolio of the Finnish waste industry offered to inter-national markets is focussed on products rather than onwaste management services. It is useful for the waste man-agement product suppliers to have information about theclients who are, in many cases, the waste management ser-vice providers. Therefore, the study analyzed this servicesector.

Waste management services are supplied by public organi-zations and private companies. This sector is highly frag-mented. There are• numerous public organizations, such as municipalities,

providing these services in their own region,• many small and medium-sized private companies being

active exclusively in small local areas• a few big players offering the services in many cases not

only in the domestic but also in foreign markets.

Therefore, the waste management product suppliers areconfronted with the challenge to serve this fragmented cli-ent sector with an adequate marketing and sales network.To support these activities the study has investigated theleading private service companies.

The Top-Ten waste management service companies in Eu-rope have a market share of 15% of the total service marketfor MSW and industrial waste. The market leaders are theFrench companies Onyx and Sita, both having a marketshare of 4%. RWE Umwelt from Germany has a marketshare of 2% and all other players have 1% or less. The de-tails are shown in Fig. 3.8.

9

9%

3%3%

10%

8%35%

20%12%

Germany19.2

France11.0

UK6.6

Italy5.5

Netherlands4.4

Austria1.7

Spain1.7

Others4.9

Waste management services (European Union, MSW)Total: 55 bill. EUR

Figure 3.7. Waste management services:Geographical markets.

Waste management service market (EU)Total market volume: 110 bill. EUR (2002)

Sita, F4,470

82%82%

4% 4% 2%

Onyx, F4,047

RWE Umwelt, D2,179

● Cleanaway, UK1,331: 1 %FCC, E1,122: 1 %Shanks, UK843: 1 %Biffa, UK720: < 1 %Rethmann, D698: < 1 %Alba, D653: < 1 %Essent, NL*543: < 1 %

●

●

●

●

●

●

* companypublic-owned

Figure 3.8. Market share of Top-Ten servicecompanies.

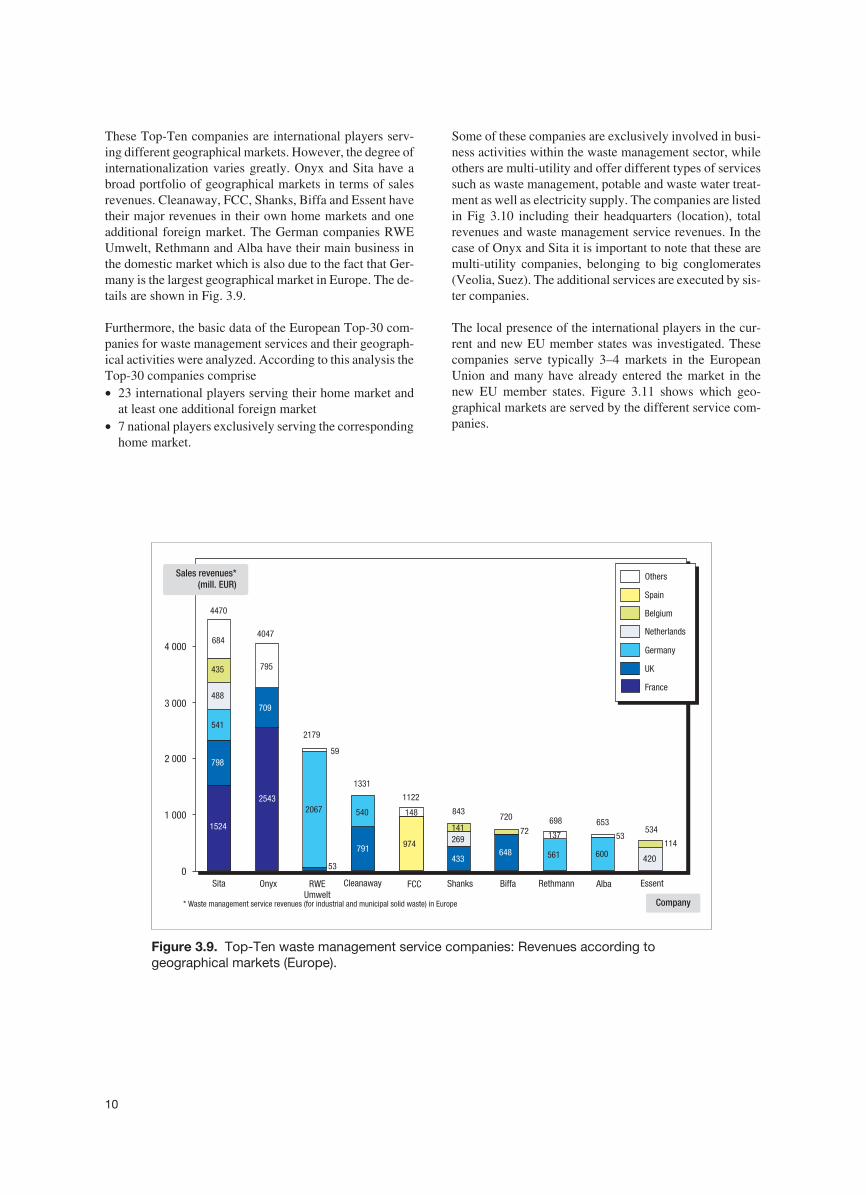

These Top-Ten companies are international players serv-ing different geographical markets. However, the degree ofinternationalization varies greatly. Onyx and Sita have abroad portfolio of geographical markets in terms of salesrevenues. Cleanaway, FCC, Shanks, Biffa and Essent havetheir major revenues in their own home markets and oneadditional foreign market. The German companies RWEUmwelt, Rethmann and Alba have their main business inthe domestic market which is also due to the fact that Ger-many is the largest geographical market in Europe. The de-tails are shown in Fig. 3.9.

Furthermore, the basic data of the European Top-30 com-panies for waste management services and their geograph-ical activities were analyzed. According to this analysis theTop-30 companies comprise• 23 international players serving their home market and

at least one additional foreign market• 7 national players exclusively serving the corresponding

home market.

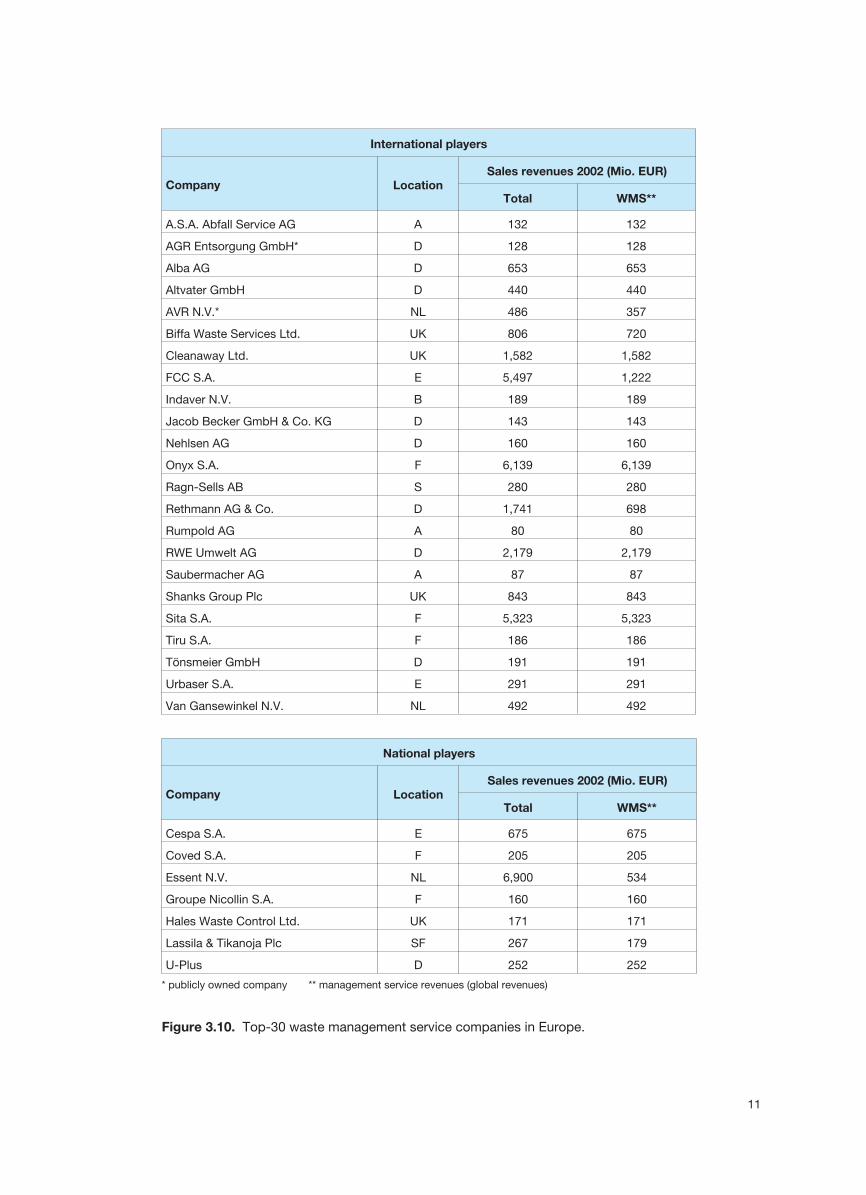

Some of these companies are exclusively involved in busi-ness activities within the waste management sector, whileothers are multi-utility and offer different types of servicessuch as waste management, potable and waste water treat-ment as well as electricity supply. The companies are listedin Fig 3.10 including their headquarters (location), totalrevenues and waste management service revenues. In thecase of Onyx and Sita it is important to note that these aremulti-utility companies, belonging to big conglomerates(Veolia, Suez). The additional services are executed by sis-ter companies.

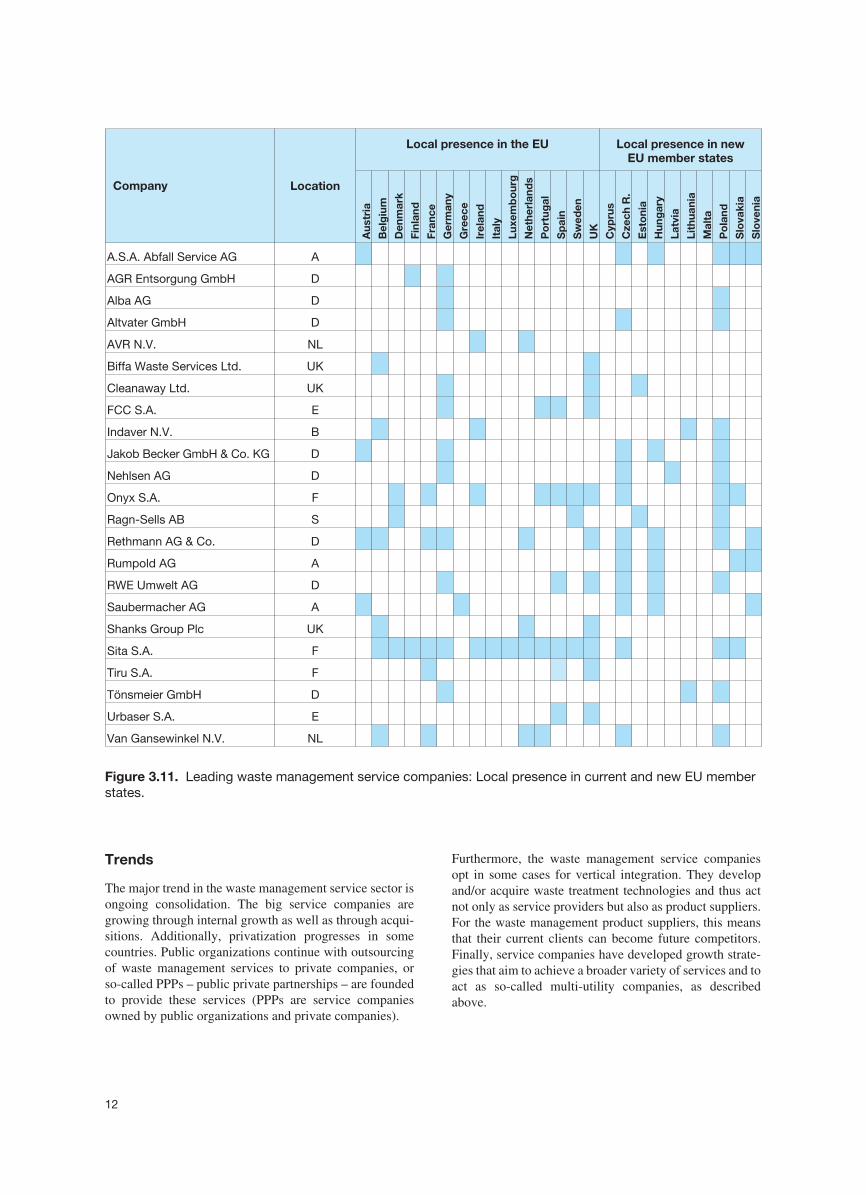

The local presence of the international players in the cur-rent and new EU member states was investigated. Thesecompanies serve typically 3–4 markets in the EuropeanUnion and many have already entered the market in thenew EU member states. Figure 3.11 shows which geo-graphical markets are served by the different service com-panies.

10

1524

2543

798

791433

648

541

2067 540

600

488

420

974

684

795

709

53561

269 114

435

141 72 137

148

53

59

0

1 000

2 000

3 000

4 000

5 000

* management service revenues (for industrial and municipal solid waste) in EuropeWaste

Sales revenues*(mill. EUR)

Belgium

Germany

UK

France

Spain

Netherlands

Others

4470

4047

2179

1122

843698720

1331

653534

Company

Sita Onyx RWEUmwelt

Cleanaway FCC Shanks EssentRethmannBiffa Alba

Figure 3.9. Top-Ten waste management service companies: Revenues according togeographical markets (Europe).

11

International players

Company LocationSales revenues 2002 (Mio. EUR)

Total WMS**

A.S.A. Abfall Service AG A 132 132

AGR Entsorgung GmbH* D 128 128

Alba AG D 653 653

Altvater GmbH D 440 440

AVR N.V.* NL 486 357

Biffa Waste Services Ltd. UK 806 720

Cleanaway Ltd. UK 1,582 1,582

FCC S.A. E 5,497 1,222

Indaver N.V. B 189 189

Jacob Becker GmbH & Co. KG D 143 143

Nehlsen AG D 160 160

Onyx S.A. F 6,139 6,139

Ragn-Sells AB S 280 280

Rethmann AG & Co. D 1,741 698

Rumpold AG A 80 80

RWE Umwelt AG D 2,179 2,179

Saubermacher AG A 87 87

Shanks Group Plc UK 843 843

Sita S.A. F 5,323 5,323

Tiru S.A. F 186 186

Tönsmeier GmbH D 191 191

Urbaser S.A. E 291 291

Van Gansewinkel N.V. NL 492 492

Figure 3.10. Top-30 waste management service companies in Europe.

National players

Company LocationSales revenues 2002 (Mio. EUR)

Total WMS**

Cespa S.A. E 675 675

Coved S.A. F 205 205

Essent N.V. NL 6,900 534

Groupe Nicollin S.A. F 160 160

Hales Waste Control Ltd. UK 171 171

Lassila & Tikanoja Plc SF 267 179

U-Plus D 252 252

* publicly owned company ** management service revenues (global revenues)

Trends

The major trend in the waste management service sector isongoing consolidation. The big service companies aregrowing through internal growth as well as through acqui-sitions. Additionally, privatization progresses in somecountries. Public organizations continue with outsourcingof waste management services to private companies, orso-called PPPs – public private partnerships – are foundedto provide these services (PPPs are service companiesowned by public organizations and private companies).

Furthermore, the waste management service companiesopt in some cases for vertical integration. They developand/or acquire waste treatment technologies and thus actnot only as service providers but also as product suppliers.For the waste management product suppliers, this meansthat their current clients can become future competitors.Finally, service companies have developed growth strate-gies that aim to achieve a broader variety of services and toact as so-called multi-utility companies, as describedabove.

12

Company Location

Local presence in the EU Local presence in newEU member states

Aus

tria

Bel

giu

m

Den

mar

k

Finl

and

Fran

ce

Ger

man

y

Gre

ece

Irel

and

Ital

y

Luxe

mb

our

g

Net

herl

and

s

Po

rtug

al

Sp

ain

Sw

eden

UK

Cyp

rus

Cze

chR

.

Est

oni

a

Hun

gar

y

Latv

ia

Lith

uani

a

Mal

ta

Po

land

Slo

vaki

a

Slo

veni

a

A.S.A. Abfall Service AG A

AGR Entsorgung GmbH D

Alba AG D

Altvater GmbH D

AVR N.V. NL

Biffa Waste Services Ltd. UK

Cleanaway Ltd. UK

FCC S.A. E

Indaver N.V. B

Jakob Becker GmbH & Co. KG D

Nehlsen AG D

Onyx S.A. F

Ragn-Sells AB S

Rethmann AG & Co. D

Rumpold AG A

RWE Umwelt AG D

Saubermacher AG A

Shanks Group Plc UK

Sita S.A. F

Tiru S.A. F

Tönsmeier GmbH D

Urbaser S.A. E

Van Gansewinkel N.V. NL

Figure 3.11. Leading waste management service companies: Local presence in current and new EU memberstates.

4 Markets for intelligent waste managementproducts and services – overview

This chapter gives an overview of the drivers for innova-tive concepts as well as the identified innovative conceptsand attractivity in terms of the market and competitive situ-ation. The details of the individual concepts are describedin Chapter 5.

Driving forces for innovative concepts

Based on the findings of this study, it can be said that envi-ronmental rules and their implementation are still the majordrivers for the development of new markets and innovativeconcepts for waste management products and services. Ad-ditionally, cost savings and quality improvements play animportant role.

Currently, the markets for mechanical biological treatmentplants, as well as for electronic scrap handling and recy-cling, are pushed by new rules of the European Union andits member states. However, the implementation of theserules differs a great deal in the various EU member states.While in some countries a market for these products al-ready exists it is not clear yet for other countries when amarket will arise.

In many EU member states, the citizens are confrontedwith steadily increasing fees for waste management overmany years. It is becoming apparent that people will nolonger accept the present price developments; therefore,waste management service providers have to look for newsolutions with lower costs. In general, cost savings can beachieved by automation of logistics and processes as wellas new solutions for collection, handling, recycling anddisposal of waste. Additionally, cost savings can beachieved through the optimization of the organizations andthe organizational processes of waste management serviceproviders.

Finally, quality improvements of products and services arealso an important driver. Examples are suction systems andautomated sorting plants. At present, waste collection is

achieved in most cases by storing waste in bins and collect-ing the bins through collection trucks. In some countries,vacuum piping systems for waste collection in office build-ings, shopping centres and residential areas have been in-troduced; these systems offer easier-to-handle systems forthe customers. Furthermore, there are ongoing discussions(e.g. in Germany) about substitution of the current complexcollection system consisting of different bins for differentwaste fractions with a new collection system with one bin(for all waste fractions) and automated sorting plants forthe waste fractions.

Innovative concepts

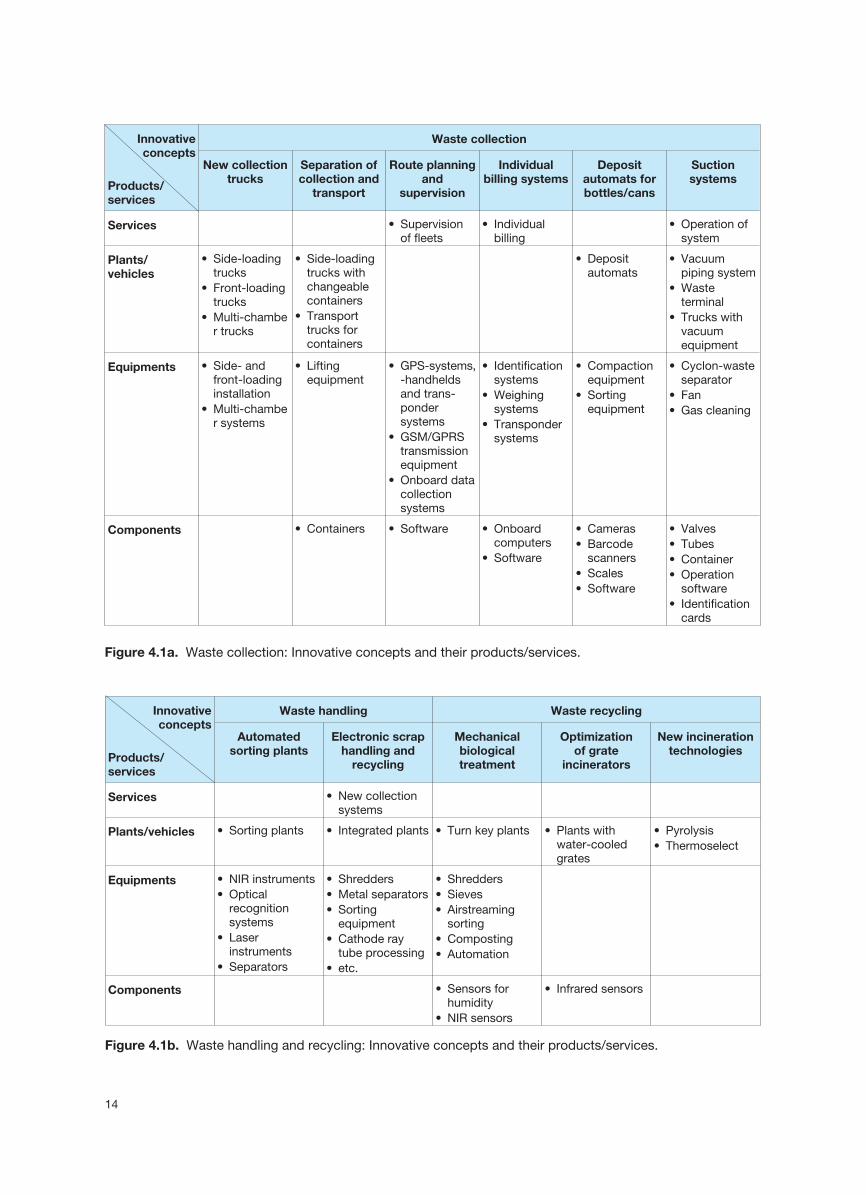

On the basis of the methodology used 11 innovative con-cepts consisting of different products and services havebeen identified. According to the process chain these are asfollows:• Waste prevention

– Biodegradable materials• Waste collection

– New collection trucks– Separation of collection and transport– Route planning and supervision– Individual billing systems– Deposit automats for bottles/cans– Suction systems

• Waste handling– Automated sorting plants– Electronic scrap handling and recycling

• Waste recycling– Mechanical biological treatment– Optimization of grate incinerators– New incineration technologies.

These innovative concepts cover a broad variety of prod-ucts and services which are shown according to individualconcepts in Fig. 4.1a for waste collection and in Fig. 4.1bfor waste handling and recycling.

13

14

Innovativeconcepts

Products/services

Waste collection

New collectiontrucks

Separation ofcollection and

transport

Route planningand

supervision

Individualbilling systems

Depositautomats forbottles/cans

Suctionsystems

Services • Supervisionof fleets

• Individualbilling

• Operation ofsystem

Plants/vehicles

• Side-loadingtrucks

• Front-loadingtrucks

• Multi-chamber trucks

• Side-loadingtrucks withchangeablecontainers

• Transporttrucks forcontainers

• Depositautomats

• Vacuumpiping system

• Wasteterminal

• Trucks withvacuumequipment

Equipments • Side- andfront-loadinginstallation

• Multi-chamber systems

• Liftingequipment

• GPS-systems,-handheldsand trans-pondersystems

• GSM/GPRStransmissionequipment

• Onboard datacollectionsystems

• Identificationsystems

• Weighingsystems

• Transpondersystems

• Compactionequipment

• Sortingequipment

• Cyclon-wasteseparator

• Fan• Gas cleaning

Components • Containers • Software • Onboardcomputers

• Software

• Cameras• Barcode

scanners• Scales• Software

• Valves• Tubes• Container• Operation

software• Identification

cards

Figure 4.1a. Waste collection: Innovative concepts and their products/services.

Innovativeconcepts

Products/services

Waste handling Waste recycling

Automatedsorting plants

Electronic scraphandling and

recycling

Mechanicalbiologicaltreatment

Optimizationof grate

incinerators

New incinerationtechnologies

Services • New collectionsystems

Plants/vehicles • Sorting plants • Integrated plants • Turn key plants • Plants withwater-cooledgrates

• Pyrolysis• Thermoselect

Equipments • NIR instruments• Optical

recognitionsystems

• Laserinstruments

• Separators

• Shredders• Metal separators• Sorting

equipment• Cathode ray

tube processing• etc.

• Shredders• Sieves• Airstreaming

sorting• Composting• Automation

Components • Sensors forhumidity

• NIR sensors

• Infrared sensors

Figure 4.1b. Waste handling and recycling: Innovative concepts and their products/services.

The following clarifications are necessary in relation to thelist of identified innovative concepts in order to avoid mis-understandings.

New and innovative concepts for waste prevention andminimization are mainly developed by the product/wasteproducers (e.g. chemical, packaging, mobile phone indus-try) and not by the waste industry. Due to the fact that thisstudy is focussing on opportunities for the Finnish wasteindustry, waste prevention can be ignored. Furthermore, itis necessary for the waste management service sector –consisting of public organizations and private companies –to increase its efficiency by investments in information andcommunication technology (ICT). However, ICT is not aproduct of the waste industry, therefore, this market wasnot investigated independently.

In conclusion, further innovative concepts may exist but,due to the chosen methodological approach, it can be as-sumed that this study covers all of the important innovativeconcepts in terms of market volume.

Attractive markets

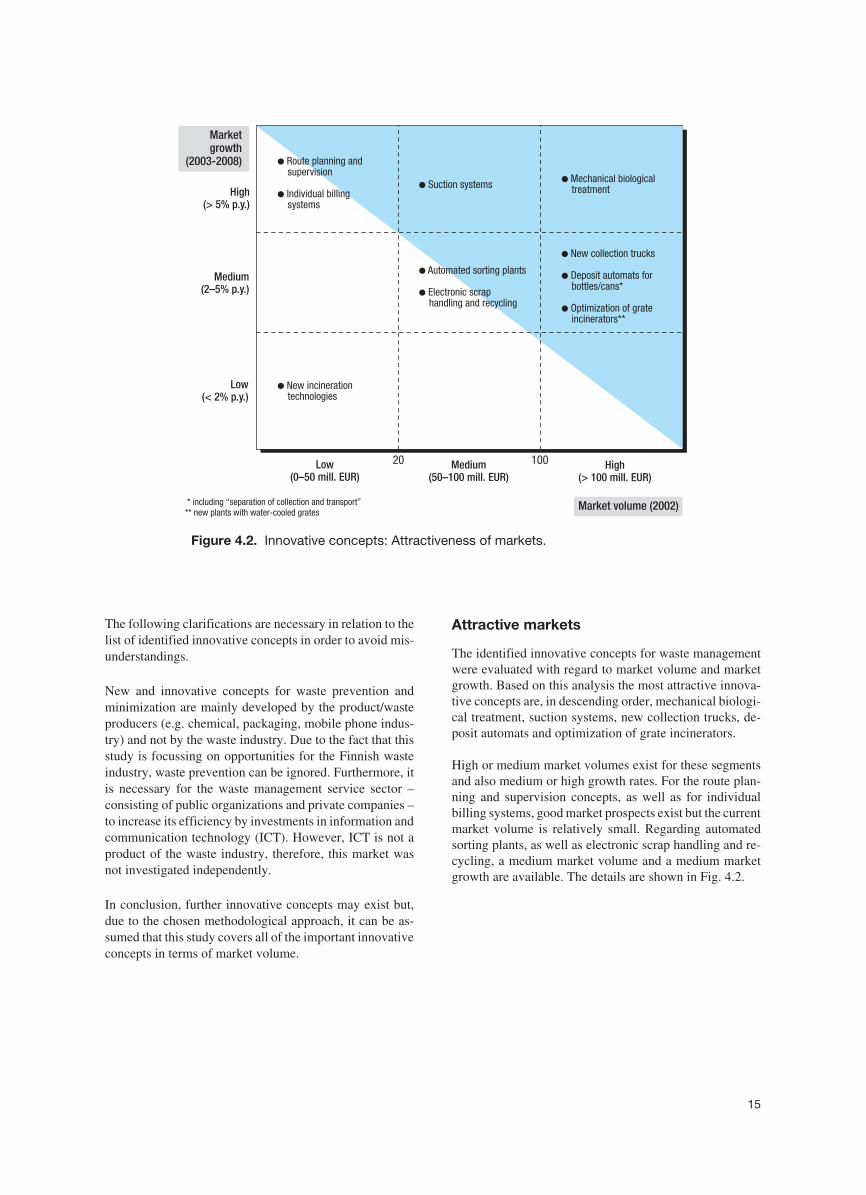

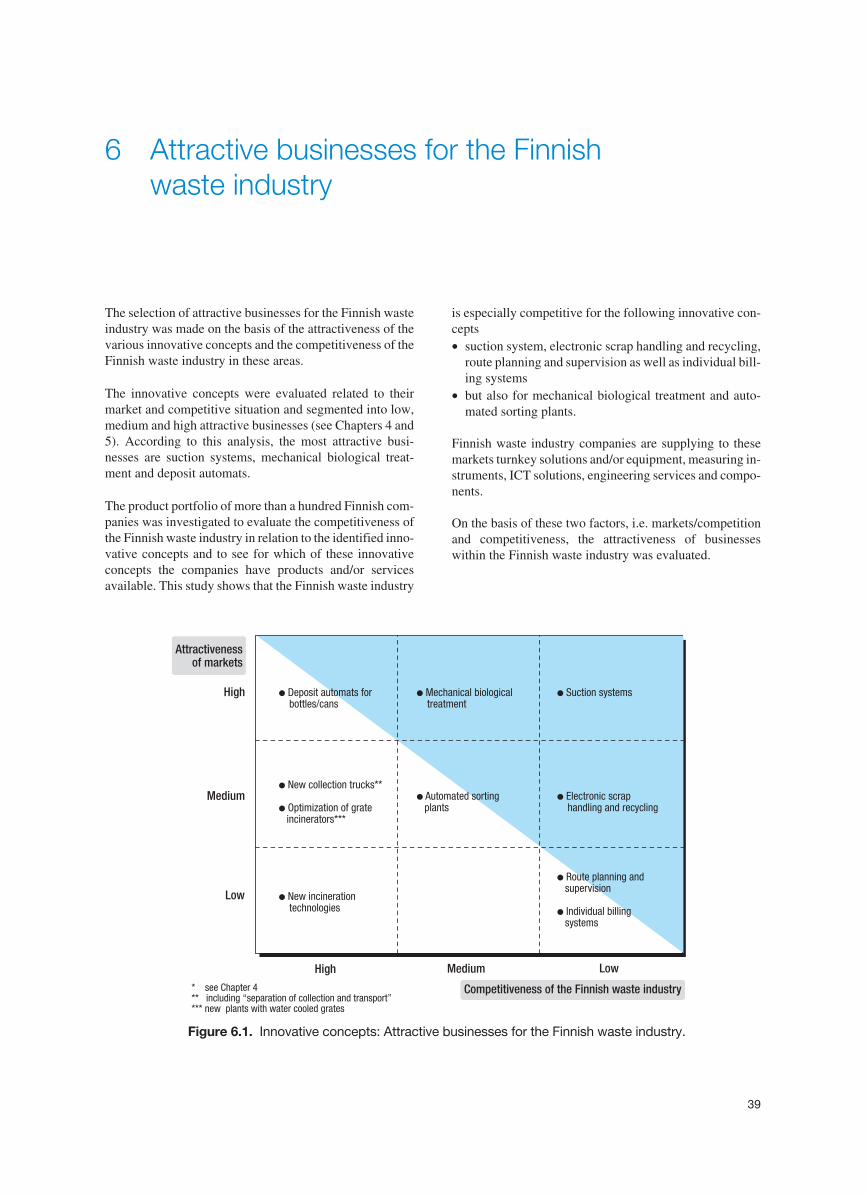

The identified innovative concepts for waste managementwere evaluated with regard to market volume and marketgrowth. Based on this analysis the most attractive innova-tive concepts are, in descending order, mechanical biologi-cal treatment, suction systems, new collection trucks, de-posit automats and optimization of grate incinerators.

High or medium market volumes exist for these segmentsand also medium or high growth rates. For the route plan-ning and supervision concepts, as well as for individualbilling systems, good market prospects exist but the currentmarket volume is relatively small. Regarding automatedsorting plants, as well as electronic scrap handling and re-cycling, a medium market volume and a medium marketgrowth are available. The details are shown in Fig. 4.2.

15

* including “separation of collection and transport”** new plants with water-cooled grates

Market volume (2002)

High(> 5% p.y.)

Medium(2–5% p.y.)

Low(< 2% p.y.)

Low(0–50 mill. EUR)

High(> 100 mill. EUR)

Marketgrowth

(2003-2008)

●

technologiesNew incineration

Medium(50–100 mill. EUR)

20 100

●

●

●

New collection trucks

Deposit automats forbottles/cans*

Optimization of grateincinerators**

● biologicaltreatmentMechanical

●

●

Route planning andsupervision

Individual billingsystems

●

●

plants

Electronic scraphandling and recycling

Automated sorting

● Suction systems

Figure 4.2. Innovative concepts: Attractiveness of markets.

Attractive businesses

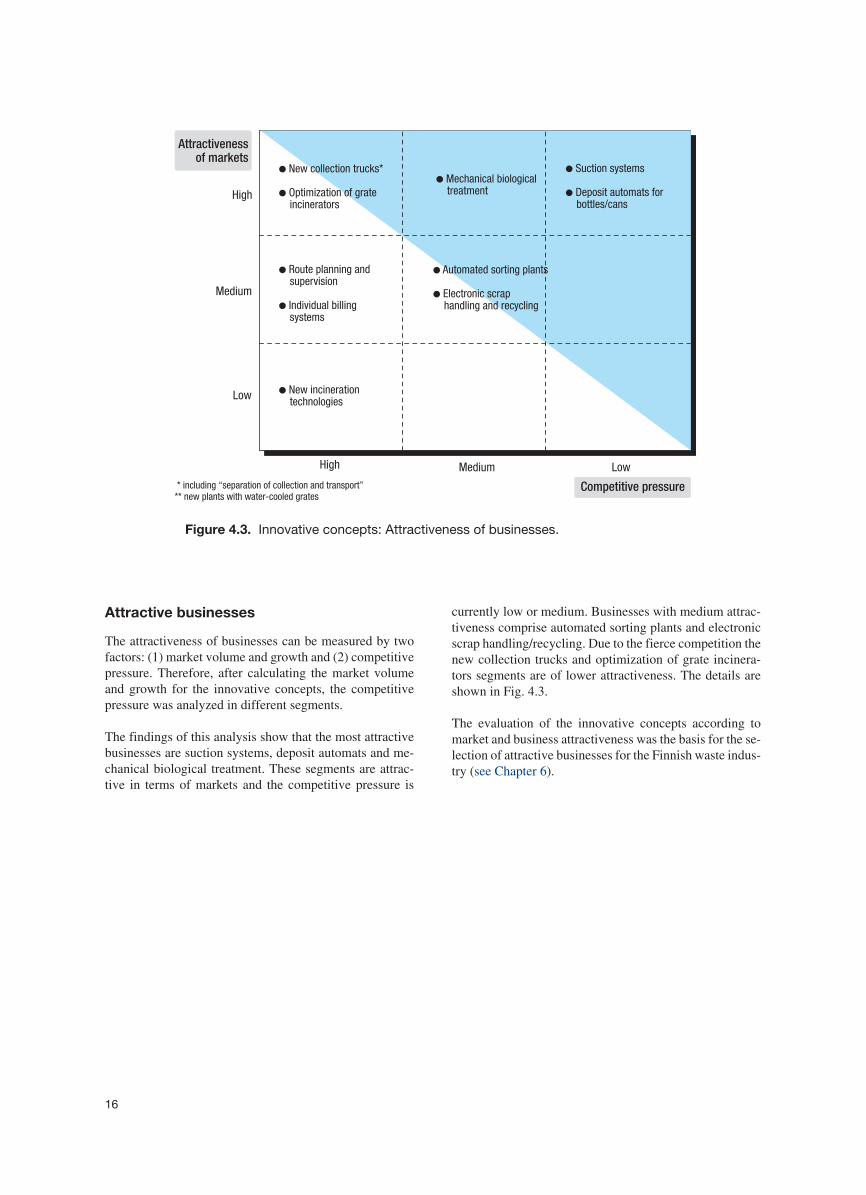

The attractiveness of businesses can be measured by twofactors: (1) market volume and growth and (2) competitivepressure. Therefore, after calculating the market volumeand growth for the innovative concepts, the competitivepressure was analyzed in different segments.

The findings of this analysis show that the most attractivebusinesses are suction systems, deposit automats and me-chanical biological treatment. These segments are attrac-tive in terms of markets and the competitive pressure is

currently low or medium. Businesses with medium attrac-tiveness comprise automated sorting plants and electronicscrap handling/recycling. Due to the fierce competition thenew collection trucks and optimization of grate incinera-tors segments are of lower attractiveness. The details areshown in Fig. 4.3.

The evaluation of the innovative concepts according tomarket and business attractiveness was the basis for the se-lection of attractive businesses for the Finnish waste indus-try (see Chapter 6).

16

High

High

Medium

Low

Medium Low

Attractivenessof markets

Competitive pressure

● tiontechnologiesNew incinera

●

● Deposit automats forbottles/cans

Suction systems●

treatmentMechanical biological

●

●

supervision

Individual billingsystems

Route planning and ●

●

plants

Electronic scraphandling and recycling

Automated sorting

●

●

trucks*

Optimization of grateincinerators

New collection

* including “separation of collection and transport”** new plants with water-cooled grates

Figure 4.3. Innovative concepts: Attractiveness of businesses.

5 Characterization of intelligent productsand services

5.1 Waste prevention

Introduction

Waste prevention means to avoid or minimize the produc-tion of waste and is a more favourable solution than wastetreatment. Waste prevention is possible to a certain extentbut it is not possible to avoid waste production altogether.

In general, measures for waste prevention are developedand executed by the waste producing industries (e.g. thechemical, packaging and electronics industry). These mea-sures lead, for example, to the development and use ofpackaging materials that are biodegradable or have a re-duced weight/volume or they lead to the reuse of productsin the electronics industry. However, the waste industry isnot normally involved in the development of waste preven-tion solutions. Therefore, the study does not focus on thisissue but investigates biodegradable materials as an exam-ple of waste prevention.

Biodegradable materials

An objective of the development and use of biodegradablematerials is to quantify the availability of products that canbe easily recycled through composting or anaerobic degra-dation. An additional advantage of these products is thatthe consumption of petroleum can be reduced because con-ventional products which are substituted by biodegradableproducts are mostly made from plastics (which are madefrom petroleum).

Biodegradable materials serve for the production of pack-aging, foil, trays, cups, plates, cutlery, pots, etc. (see Fig.5.1). So far, thermoplastics are used for these products inmost cases.

Biodegradable materials are made from• natural materials such as starch from corn, wheat,

potatoes, cellulose and sugars,• synthetic materials consisting of aliphatic-aromatic

esters.

The biodegradable materials and products are developedand supplied by the chemical and starch industry and spe-cialized companies. Examples of companies that are activein this area are the following:• Chemical, starch industry

– Germany: BASF, Compopure– Italy: Novamont

• Specialized companies– Germany: Biologische Naturverpackungen,

Natura Verpackung, Trespaphan– the Netherlands: Rodenburg Biopolymers.

The use of biodegradable materials will increase steadily inthe future according to experts and material suppliers.

17

Figure 5.1. Biodegradable materials and products.

5.2 Waste collection

5.2.1 New collection trucks

Introduction

The vast majority of private households in Europe collectand sort waste in bins. In some instances, one bin is usedfor all types of waste, whereas in others various bins areused for different waste fractions, for example paper,biowaste and residual waste.

Traditionally, these bins are collected by rear-loadingtrucks with a single chamber/container. This type of collec-tion truck requires at least two workers: one of them has todrive the truck, and the other one collects and empties thebins. There is often more than one worker employed in theactual collection process, depending on the individual col-lection situation (corresponding to the number of bins, thedistance from truck to bins, etc.).

With rear-loading trucks, each bin is placed manually on alifter at the rear end of the truck by the collection worker.The bin is lifted by the lifting equipment and emptied intothe truck‘s container. This process is controlled by theworker employing control units. The emptied bins have tobe put back on the sidewalk.

Using traditional rear-loading trucks for the collection ofMSW leads to high costs for two main reasons:

• High personnel costsFor the collection of MSW with rear-loading trucks atleast two, but often more, persons are needed per truck.

• Manifold collection runsIn general, rear-loading collection trucks have onechamber/container. Therefore, with one run, only onewaste fraction can be collected. In cases where differentwaste fractions (in different bins) are collected by theprivate households, double or threefold collection runsare necessary. This is time consuming and creates highcosts.

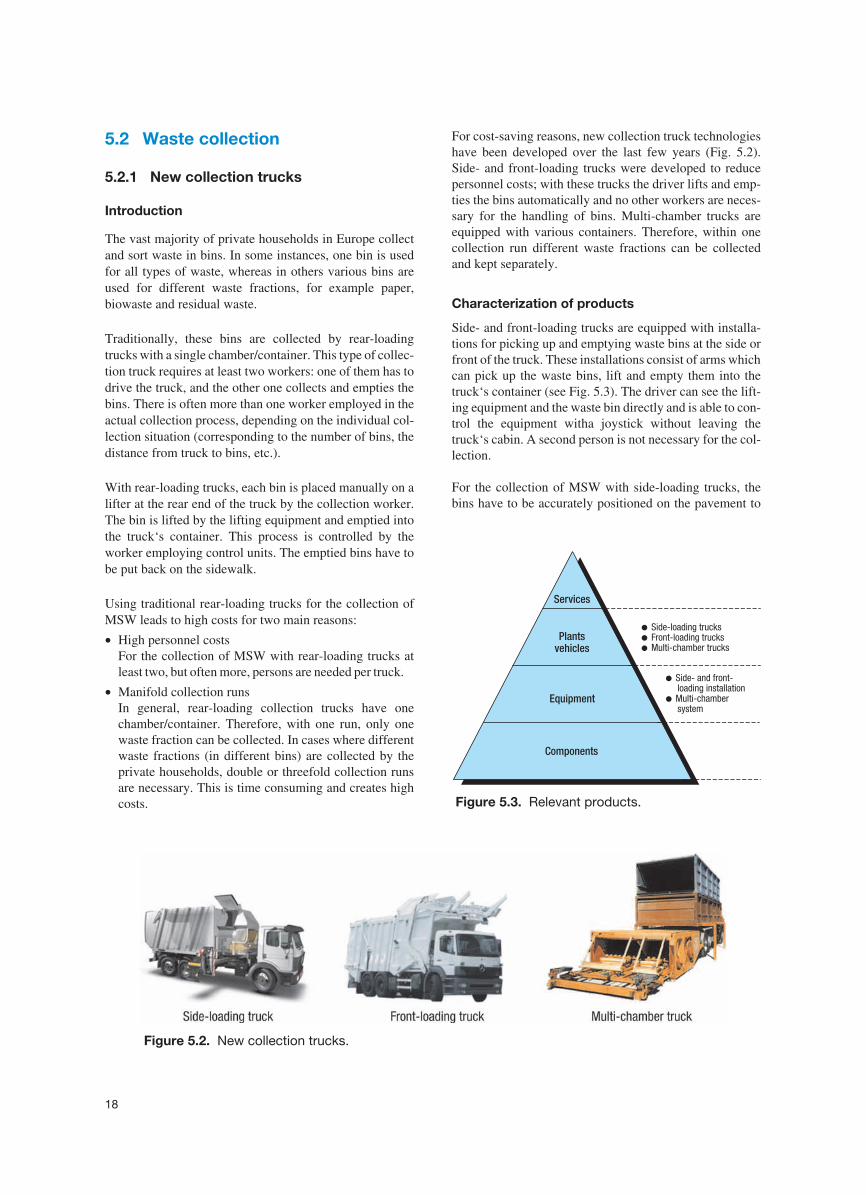

For cost-saving reasons, new collection truck technologieshave been developed over the last few years (Fig. 5.2).Side- and front-loading trucks were developed to reducepersonnel costs; with these trucks the driver lifts and emp-ties the bins automatically and no other workers are neces-sary for the handling of bins. Multi-chamber trucks areequipped with various containers. Therefore, within onecollection run different waste fractions can be collectedand kept separately.

Characterization of products

Side- and front-loading trucks are equipped with installa-tions for picking up and emptying waste bins at the side orfront of the truck. These installations consist of arms whichcan pick up the waste bins, lift and empty them into thetruck‘s container (see Fig. 5.3). The driver can see the lift-ing equipment and the waste bin directly and is able to con-trol the equipment witha joystick without leaving thetruck‘s cabin. A second person is not necessary for the col-lection.

For the collection of MSW with side-loading trucks, thebins have to be accurately positioned on the pavement to

18

Figure 5.2. New collection trucks.

Equipment

Services

Plantsvehicles

Components

●

●

●

Side-loading trucksFront-loading trucksMulti-chamber trucks

● - and front-loading installationMulti-chambersystem

Side

●

Figure 5.3. Relevant products.

enable the grabbing of the bin by the truck‘s arm. Thewaste bin is picked up, lifted and emptied sideways.

With front-loading trucks, the bins are picked up from thefront of the truck, lifted over the driver‘s cabin and emptiedinto the truck‘s container from above.

Multi-chamber trucks are equipped with two, three or fourseparate containers for separate waste fractions. For liftingand emptying of the waste bins, special lifters are usedwhich enable the filling of waste fractions in the respectivewaste containers. In this way the number of collection runsfor different waste fractions can be reduced.

Pros and cons

Side- and front-loading trucks offer personnel cost sav-ings compared to conventional rear-loading trucks becauseone person is able to empty the bins.

On the other hand there are higher investment costs fortrucks equipped with these technologies. The average pricelevel is as follows:• Side-loading truck: 220,000 EUR• Front-loading truck: 180,000 EUR• Rear-loading truck: 140,000 EUR

Additionally, the usefulness of these trucks can be some-what limited, especially in cities, due to problems that oc-cur when bins are not properly positioned for collection orwhen they are blocked by parked cars.

According to leading waste management companies, theside-loading truck is used mainly in rural areas and in citieswith an infrastructure well suited for this technology. Fur-thermore, major truck manufacturers predict that theside-loading truck will not be able to completely replacethe rear-loading truck in cities.

In general, according to major waste service companies,front-loading trucks are not used for municipal solid wastebut for industrial and specific commercial waste.

Multi-chamber trucks offer cost savings due to reducedcollection costs which result from a reduced number of col-lection runs.

On the other hand these types of trucks have major disad-vantages. Problems are caused by the different specificweights of the waste fractions when chambers are arrangedvertically.

The major problem is the low overall filling degree of thechambers due to the different volumes of waste fractionswhich cannot be predicted or calculated precisely in ad-vance. As a result, the truck has to stop the collection runwhen one of the chambers is full. Therefore, the theoreticaladvantage is lost in many cases.

We can conclude that multi-chamber trucks will not beused in the future due to these disadvantages. According toleading waste management service companiesmulti-chamber trucks do not have any future in the MSWcollection business.

Market outlook

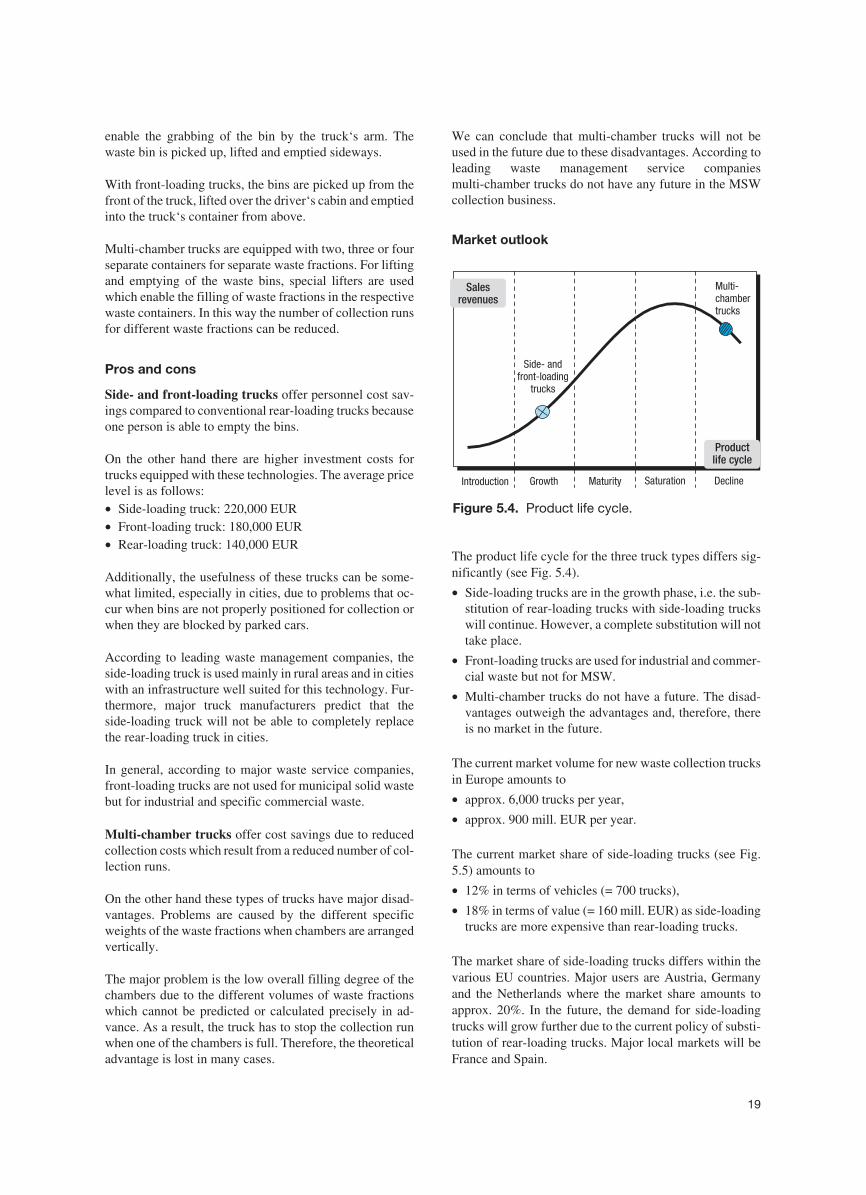

The product life cycle for the three truck types differs sig-nificantly (see Fig. 5.4).

• Side-loading trucks are in the growth phase, i.e. the sub-stitution of rear-loading trucks with side-loading truckswill continue. However, a complete substitution will nottake place.

• Front-loading trucks are used for industrial and commer-cial waste but not for MSW.

• Multi-chamber trucks do not have a future. The disad-vantages outweigh the advantages and, therefore, thereis no market in the future.

The current market volume for new waste collection trucksin Europe amounts to

• approx. 6,000 trucks per year,

• approx. 900 mill. EUR per year.

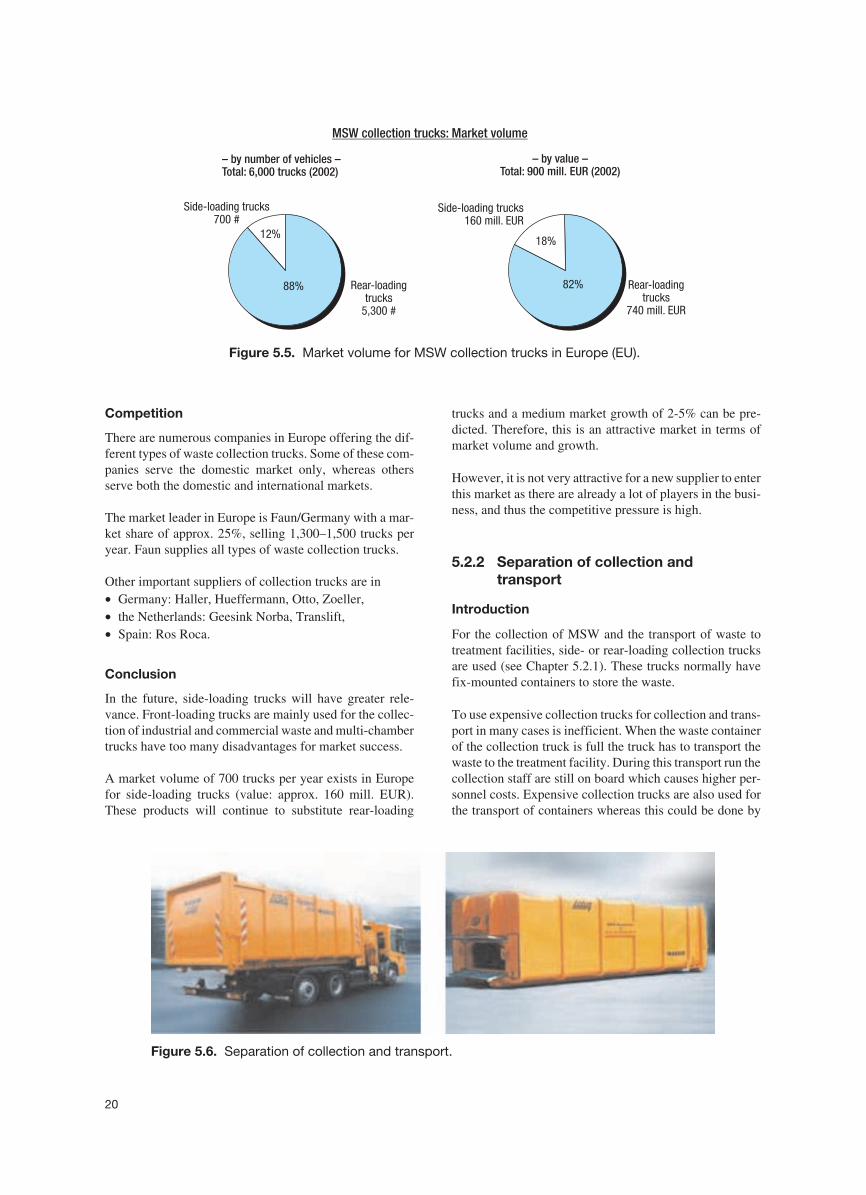

The current market share of side-loading trucks (see Fig.5.5) amounts to

• 12% in terms of vehicles (= 700 trucks),

• 18% in terms of value (= 160 mill. EUR) as side-loadingtrucks are more expensive than rear-loading trucks.

The market share of side-loading trucks differs within thevarious EU countries. Major users are Austria, Germanyand the Netherlands where the market share amounts toapprox. 20%. In the future, the demand for side-loadingtrucks will grow further due to the current policy of substi-tution of rear-loading trucks. Major local markets will beFrance and Spain.

19

Introduction Growth Maturity Saturation Decline

Multi-chambertrucks

Side- andfront-loading

trucks

Salesrevenues

Productlife cycle

Figure 5.4. Product life cycle.

Competition

There are numerous companies in Europe offering the dif-ferent types of waste collection trucks. Some of these com-panies serve the domestic market only, whereas othersserve both the domestic and international markets.

The market leader in Europe is Faun/Germany with a mar-ket share of approx. 25%, selling 1,300–1,500 trucks peryear. Faun supplies all types of waste collection trucks.

Other important suppliers of collection trucks are in• Germany: Haller, Hueffermann, Otto, Zoeller,• the Netherlands: Geesink Norba, Translift,• Spain: Ros Roca.

Conclusion

In the future, side-loading trucks will have greater rele-vance. Front-loading trucks are mainly used for the collec-tion of industrial and commercial waste and multi-chambertrucks have too many disadvantages for market success.

A market volume of 700 trucks per year exists in Europefor side-loading trucks (value: approx. 160 mill. EUR).These products will continue to substitute rear-loading

trucks and a medium market growth of 2-5% can be pre-dicted. Therefore, this is an attractive market in terms ofmarket volume and growth.

However, it is not very attractive for a new supplier to enterthis market as there are already a lot of players in the busi-ness, and thus the competitive pressure is high.

5.2.2 Separation of collection andtransport

Introduction

For the collection of MSW and the transport of waste totreatment facilities, side- or rear-loading collection trucksare used (see Chapter 5.2.1). These trucks normally havefix-mounted containers to store the waste.

To use expensive collection trucks for collection and trans-port in many cases is inefficient. When the waste containerof the collection truck is full the truck has to transport thewaste to the treatment facility. During this transport run thecollection staff are still on board which causes higher per-sonnel costs. Expensive collection trucks are also used forthe transport of containers whereas this could be done by

20

Figure 5.6. Separation of collection and transport.

88%

12%

Rear-loadingtrucks

5,300 #

Side-loading trucks700 #

82%

18%

Rear-loadingtrucks

740 mill. EUR

Side-loading trucks160 mill. EUR

– by number of vehicles –Total: 6,000 trucks (2002)

– by value –Total: 900 mill. EUR (2002)

MSW collection trucks: Market volume

Figure 5.5. Market volume for MSW collection trucks in Europe (EU).

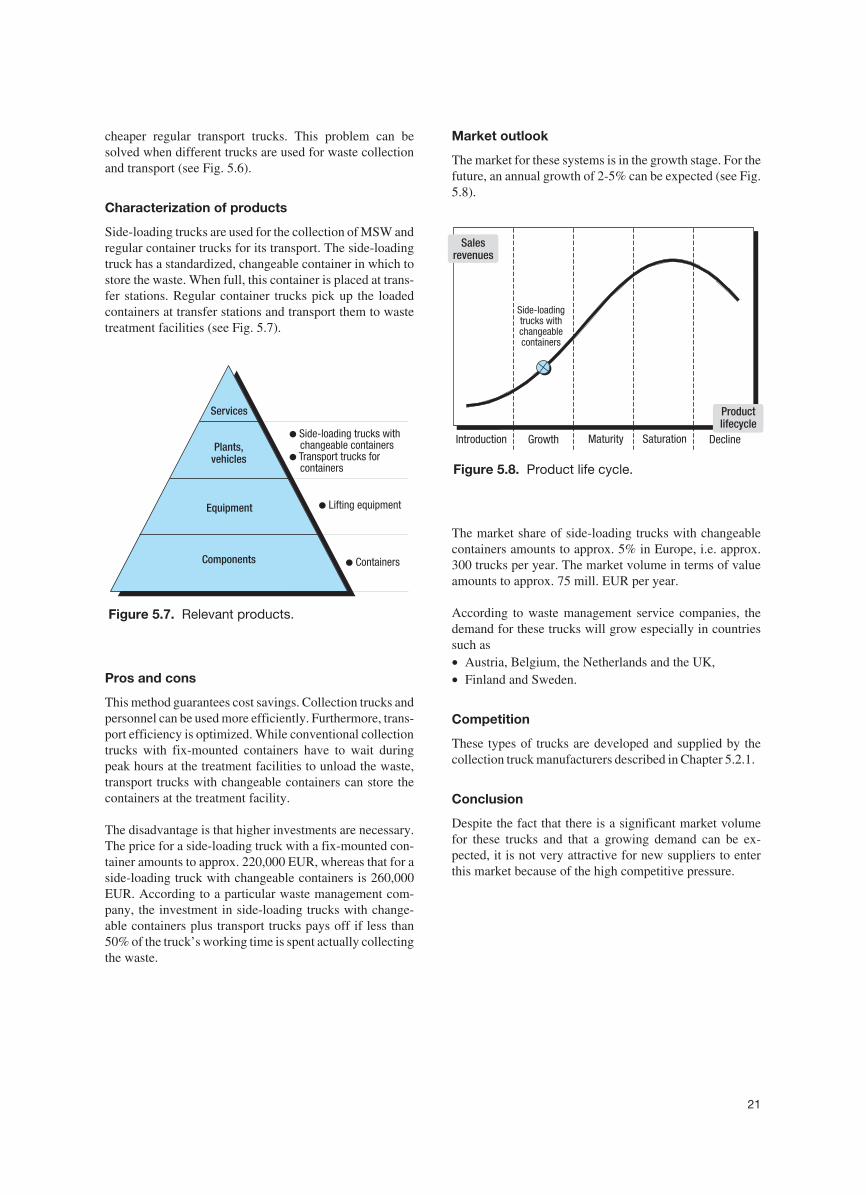

cheaper regular transport trucks. This problem can besolved when different trucks are used for waste collectionand transport (see Fig. 5.6).

Characterization of products

Side-loading trucks are used for the collection of MSW andregular container trucks for its transport. The side-loadingtruck has a standardized, changeable container in which tostore the waste. When full, this container is placed at trans-fer stations. Regular container trucks pick up the loadedcontainers at transfer stations and transport them to wastetreatment facilities (see Fig. 5.7).

Pros and cons

This method guarantees cost savings. Collection trucks andpersonnel can be used more efficiently. Furthermore, trans-port efficiency is optimized. While conventional collectiontrucks with fix-mounted containers have to wait duringpeak hours at the treatment facilities to unload the waste,transport trucks with changeable containers can store thecontainers at the treatment facility.

The disadvantage is that higher investments are necessary.The price for a side-loading truck with a fix-mounted con-tainer amounts to approx. 220,000 EUR, whereas that for aside-loading truck with changeable containers is 260,000EUR. According to a particular waste management com-pany, the investment in side-loading trucks with change-able containers plus transport trucks pays off if less than50% of the truck’s working time is spent actually collectingthe waste.

Market outlook

The market for these systems is in the growth stage. For thefuture, an annual growth of 2-5% can be expected (see Fig.5.8).

The market share of side-loading trucks with changeablecontainers amounts to approx. 5% in Europe, i.e. approx.300 trucks per year. The market volume in terms of valueamounts to approx. 75 mill. EUR per year.

According to waste management service companies, thedemand for these trucks will grow especially in countriessuch as• Austria, Belgium, the Netherlands and the UK,• Finland and Sweden.

Competition

These types of trucks are developed and supplied by thecollection truck manufacturers described in Chapter 5.2.1.

Conclusion

Despite the fact that there is a significant market volumefor these trucks and that a growing demand can be ex-pected, it is not very attractive for new suppliers to enterthis market because of the high competitive pressure.

21

● Lifting equipmentEquipment

Services

Plants,vehicles

Components

●

●

Side-loading trucks withchangeable containersTransport trucks forcontainers

● Containers

Figure 5.7. Relevant products.

Introduction Growth Maturity Saturation Decline

Productlifecycle

Side-loadingtrucks withchangeablecontainers

Salesrevenues

Figure 5.8. Product life cycle.

5.2.3 Route planning and supervision

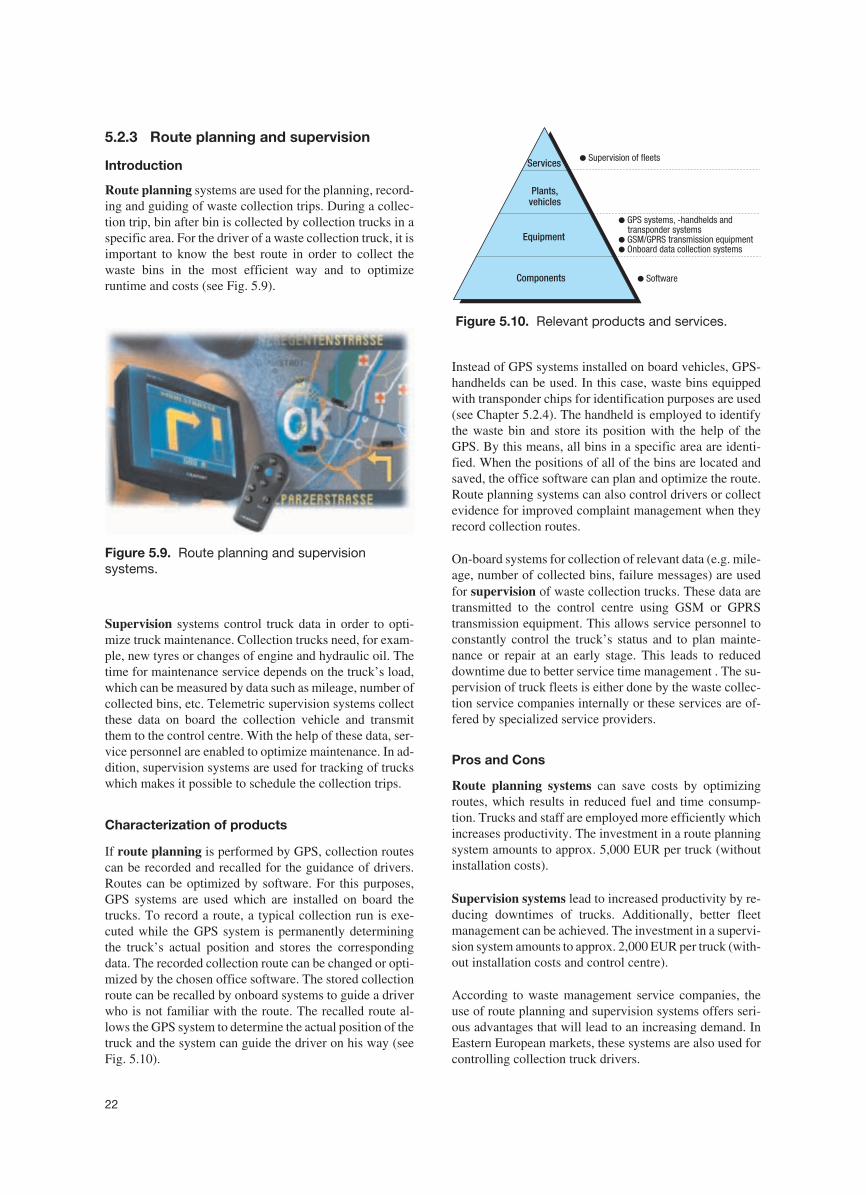

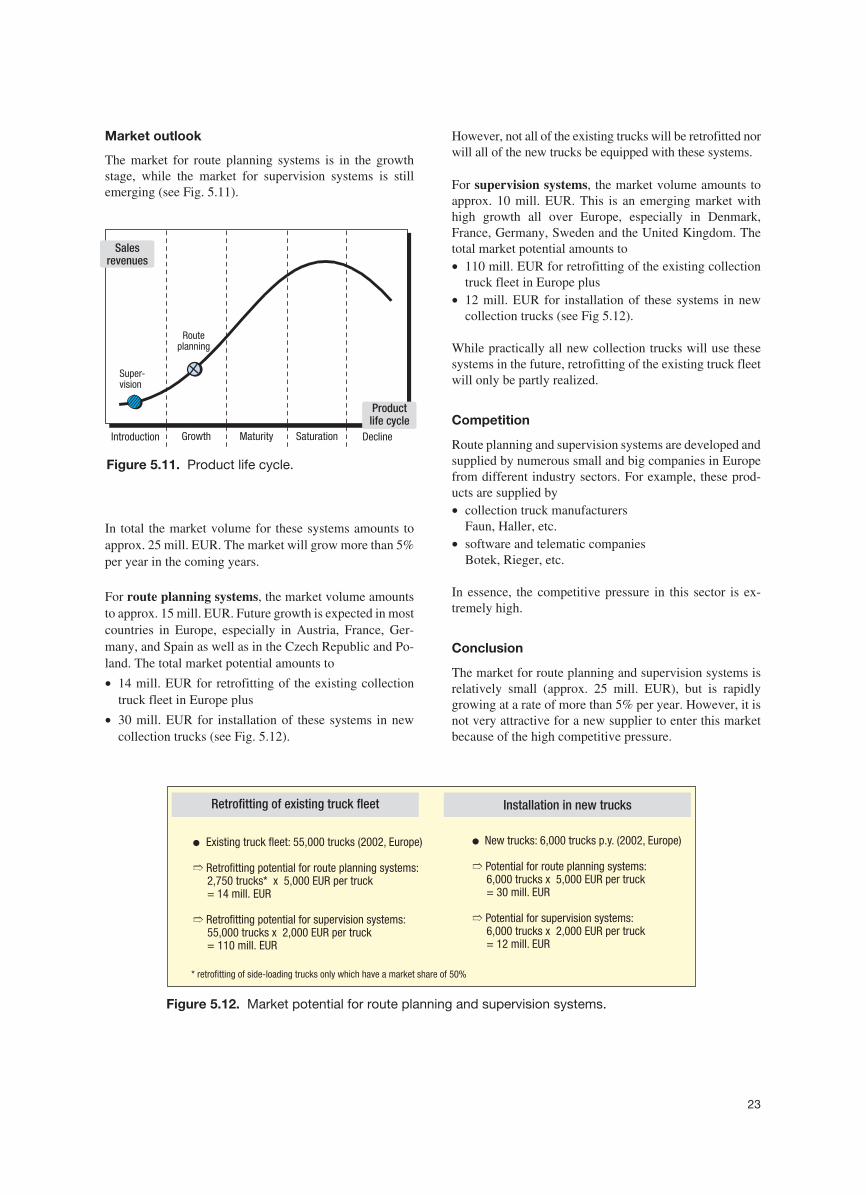

Introduction

Route planning systems are used for the planning, record-ing and guiding of waste collection trips. During a collec-tion trip, bin after bin is collected by collection trucks in aspecific area. For the driver of a waste collection truck, it isimportant to know the best route in order to collect thewaste bins in the most efficient way and to optimizeruntime and costs (see Fig. 5.9).

Supervision systems control truck data in order to opti-mize truck maintenance. Collection trucks need, for exam-ple, new tyres or changes of engine and hydraulic oil. Thetime for maintenance service depends on the truck’s load,which can be measured by data such as mileage, number ofcollected bins, etc. Telemetric supervision systems collectthese data on board the collection vehicle and transmitthem to the control centre. With the help of these data, ser-vice personnel are enabled to optimize maintenance. In ad-dition, supervision systems are used for tracking of truckswhich makes it possible to schedule the collection trips.

Characterization of products

If route planning is performed by GPS, collection routescan be recorded and recalled for the guidance of drivers.Routes can be optimized by software. For this purposes,GPS systems are used which are installed on board thetrucks. To record a route, a typical collection run is exe-cuted while the GPS system is permanently determiningthe truck’s actual position and stores the correspondingdata. The recorded collection route can be changed or opti-mized by the chosen office software. The stored collectionroute can be recalled by onboard systems to guide a driverwho is not familiar with the route. The recalled route al-lows the GPS system to determine the actual position of thetruck and the system can guide the driver on his way (seeFig. 5.10).

Instead of GPS systems installed on board vehicles, GPS-handhelds can be used. In this case, waste bins equippedwith transponder chips for identification purposes are used(see Chapter 5.2.4). The handheld is employed to identifythe waste bin and store its position with the help of theGPS. By this means, all bins in a specific area are identi-fied. When the positions of all of the bins are located andsaved, the office software can plan and optimize the route.Route planning systems can also control drivers or collectevidence for improved complaint management when theyrecord collection routes.

On-board systems for collection of relevant data (e.g. mile-age, number of collected bins, failure messages) are usedfor supervision of waste collection trucks. These data aretransmitted to the control centre using GSM or GPRStransmission equipment. This allows service personnel toconstantly control the truck’s status and to plan mainte-nance or repair at an early stage. This leads to reduceddowntime due to better service time management . The su-pervision of truck fleets is either done by the waste collec-tion service companies internally or these services are of-fered by specialized service providers.

Pros and Cons

Route planning systems can save costs by optimizingroutes, which results in reduced fuel and time consump-tion. Trucks and staff are employed more efficiently whichincreases productivity. The investment in a route planningsystem amounts to approx. 5,000 EUR per truck (withoutinstallation costs).

Supervision systems lead to increased productivity by re-ducing downtimes of trucks. Additionally, better fleetmanagement can be achieved. The investment in a supervi-sion system amounts to approx. 2,000 EUR per truck (with-out installation costs and control centre).

According to waste management service companies, theuse of route planning and supervision systems offers seri-ous advantages that will lead to an increasing demand. InEastern European markets, these systems are also used forcontrolling collection truck drivers.

22

Figure 5.9. Route planning and supervisionsystems.

Equipment

Services

Plants,vehicles

Components

● Supervision of fleets

●

●●

GPS systems, -handhelds andtransponder systemsGSM/GPRS transmission equipmentOnboard data collection systems

● Software

Figure 5.10. Relevant products and services.

Market outlook

The market for route planning systems is in the growthstage, while the market for supervision systems is stillemerging (see Fig. 5.11).

In total the market volume for these systems amounts toapprox. 25 mill. EUR. The market will grow more than 5%per year in the coming years.

For route planning systems, the market volume amountsto approx. 15 mill. EUR. Future growth is expected in mostcountries in Europe, especially in Austria, France, Ger-many, and Spain as well as in the Czech Republic and Po-land. The total market potential amounts to

• 14 mill. EUR for retrofitting of the existing collectiontruck fleet in Europe plus

• 30 mill. EUR for installation of these systems in newcollection trucks (see Fig. 5.12).

However, not all of the existing trucks will be retrofitted norwill all of the new trucks be equipped with these systems.

For supervision systems, the market volume amounts toapprox. 10 mill. EUR. This is an emerging market withhigh growth all over Europe, especially in Denmark,France, Germany, Sweden and the United Kingdom. Thetotal market potential amounts to• 110 mill. EUR for retrofitting of the existing collection

truck fleet in Europe plus• 12 mill. EUR for installation of these systems in new

collection trucks (see Fig 5.12).

While practically all new collection trucks will use thesesystems in the future, retrofitting of the existing truck fleetwill only be partly realized.

Competition

Route planning and supervision systems are developed andsupplied by numerous small and big companies in Europefrom different industry sectors. For example, these prod-ucts are supplied by• collection truck manufacturers

Faun, Haller, etc.• software and telematic companies

Botek, Rieger, etc.

In essence, the competitive pressure in this sector is ex-tremely high.

Conclusion

The market for route planning and supervision systems isrelatively small (approx. 25 mill. EUR), but is rapidlygrowing at a rate of more than 5% per year. However, it isnot very attractive for a new supplier to enter this marketbecause of the high competitive pressure.

23

Retrofitting of existing truck fleet Installation in new trucks

● Existing truck fleet: 55,000 trucks (2002, Europe)

Retrofitting potential for route planning systems:2,750 trucks* x 5,000 EUR per truck= 14 mill. EUR

Retrofitting potential for supervision systems:55,000 trucks x 2,000 EUR per truck= 110 mill. EUR

➱

➱

●

Potential for route planning systems:6,000 trucks x 5,000 EUR per truck= 30 mill. EUR

Potential for supervision systems:6,000 trucks x 2,000 EUR per truck= 12 mill. EUR

➱

➱

New trucks: 6,000 trucks p.y. (2002, Europe)

* side-loading trucks only which have a market share of 50%retrofitting of

Figure 5.12. Market potential for route planning and supervision systems.

Introduction Growth Maturity Saturation Decline

Super-vision

Routeplanning

Salesrevenues

Productlife cycle

Figure 5.11. Product life cycle.

5.2.4 Individual billing systems

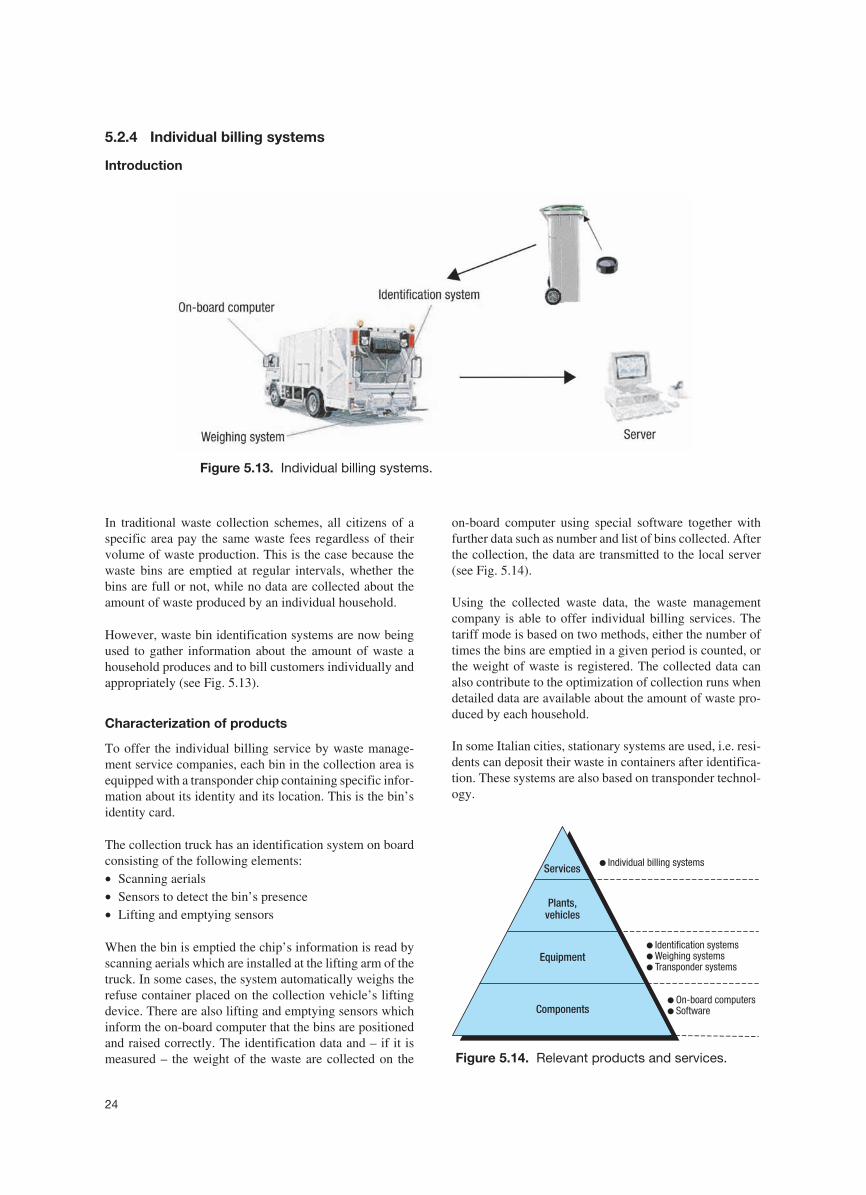

Introduction

In traditional waste collection schemes, all citizens of aspecific area pay the same waste fees regardless of theirvolume of waste production. This is the case because thewaste bins are emptied at regular intervals, whether thebins are full or not, while no data are collected about theamount of waste produced by an individual household.

However, waste bin identification systems are now beingused to gather information about the amount of waste ahousehold produces and to bill customers individually andappropriately (see Fig. 5.13).

Characterization of products

To offer the individual billing service by waste manage-ment service companies, each bin in the collection area isequipped with a transponder chip containing specific infor-mation about its identity and its location. This is the bin’sidentity card.

The collection truck has an identification system on boardconsisting of the following elements:• Scanning aerials• Sensors to detect the bin’s presence• Lifting and emptying sensors

When the bin is emptied the chip’s information is read byscanning aerials which are installed at the lifting arm of thetruck. In some cases, the system automatically weighs therefuse container placed on the collection vehicle’s liftingdevice. There are also lifting and emptying sensors whichinform the on-board computer that the bins are positionedand raised correctly. The identification data and – if it ismeasured – the weight of the waste are collected on the

on-board computer using special software together withfurther data such as number and list of bins collected. Afterthe collection, the data are transmitted to the local server(see Fig. 5.14).

Using the collected waste data, the waste managementcompany is able to offer individual billing services. Thetariff mode is based on two methods, either the number oftimes the bins are emptied in a given period is counted, orthe weight of waste is registered. The collected data canalso contribute to the optimization of collection runs whendetailed data are available about the amount of waste pro-duced by each household.

In some Italian cities, stationary systems are used, i.e. resi-dents can deposit their waste in containers after identifica-tion. These systems are also based on transponder technol-ogy.

24

Figure 5.13. Individual billing systems.

Equipment

Services

Plants,vehicles

Components

● Identification systems●

●

Weighing systemsTransponder systems

● Individual billing systems

●

●

computersSoftwareOn-board

Figure 5.14. Relevant products and services.

Pros and Cons

The principal advantage of individual billing systems is thefairness of the system. Individual billing implements the“polluter pays” principle. People with higher waste pro-duction are obliged to pay higher fees. An additional posi-tive result is decreasing waste volumes due to the fact thatwaste prevention by citizens is rewarded with lower fees.

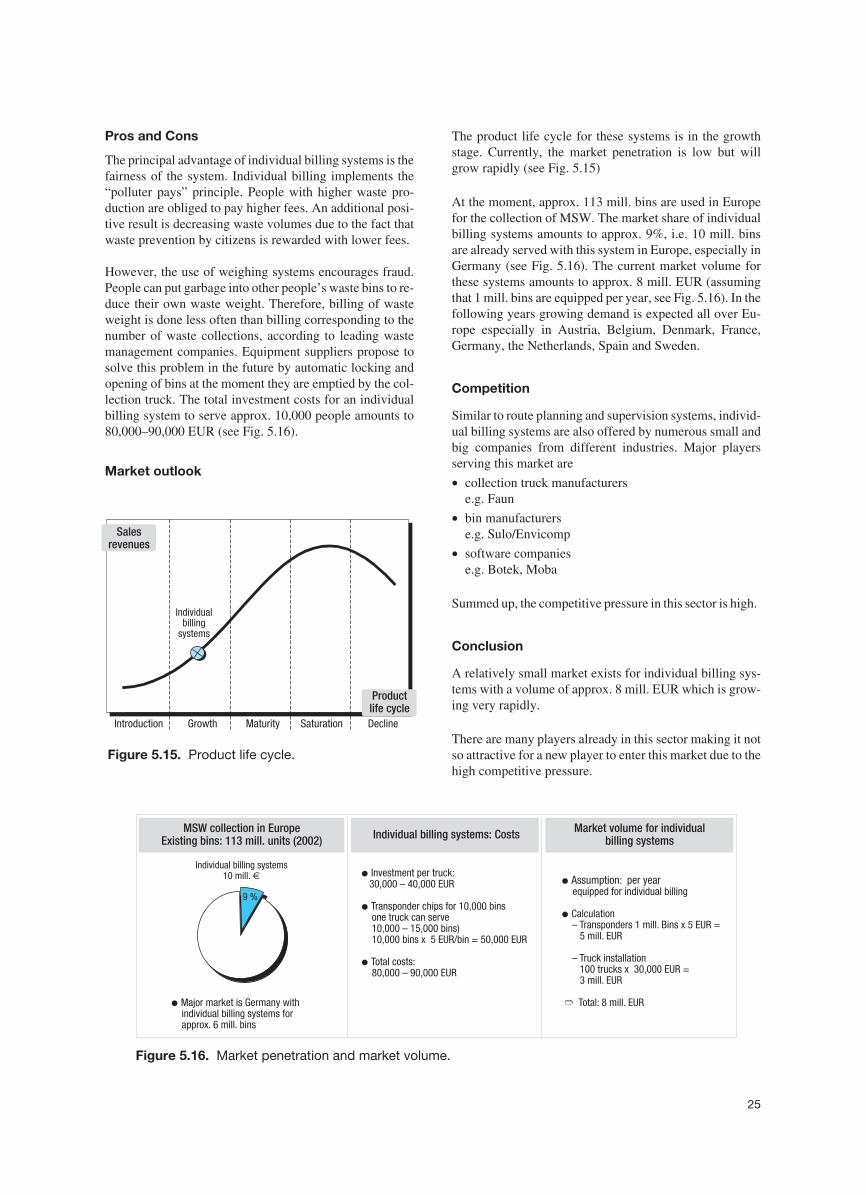

However, the use of weighing systems encourages fraud.People can put garbage into other people’s waste bins to re-duce their own waste weight. Therefore, billing of wasteweight is done less often than billing corresponding to thenumber of waste collections, according to leading wastemanagement companies. Equipment suppliers propose tosolve this problem in the future by automatic locking andopening of bins at the moment they are emptied by the col-lection truck. The total investment costs for an individualbilling system to serve approx. 10,000 people amounts to80,000–90,000 EUR (see Fig. 5.16).

Market outlook

The product life cycle for these systems is in the growthstage. Currently, the market penetration is low but willgrow rapidly (see Fig. 5.15)

At the moment, approx. 113 mill. bins are used in Europefor the collection of MSW. The market share of individualbilling systems amounts to approx. 9%, i.e. 10 mill. binsare already served with this system in Europe, especially inGermany (see Fig. 5.16). The current market volume forthese systems amounts to approx. 8 mill. EUR (assumingthat 1 mill. bins are equipped per year, see Fig. 5.16). In thefollowing years growing demand is expected all over Eu-rope especially in Austria, Belgium, Denmark, France,Germany, the Netherlands, Spain and Sweden.

Competition

Similar to route planning and supervision systems, individ-ual billing systems are also offered by numerous small andbig companies from different industries. Major playersserving this market are

• collection truck manufacturerse.g. Faun

• bin manufacturerse.g. Sulo/Envicomp

• software companiese.g. Botek, Moba

Summed up, the competitive pressure in this sector is high.

Conclusion

A relatively small market exists for individual billing sys-tems with a volume of approx. 8 mill. EUR which is grow-ing very rapidly.

There are many players already in this sector making it notso attractive for a new player to enter this market due to thehigh competitive pressure.

25

Introduction Growth Maturity Saturation Decline

Individualbilling

systems

Salesrevenues

Productlife cycle

Figure 5.15. Product life cycle.

●

●

●

Investment per truck:30,000 – 40,000 EUR

Transponder chips for 10,000 binsone truck can serve10,000 – 15,000 bins)10,000 bins x 5 EUR/bin = 50,000 EUR

Total costs:80,000 – 90,000 EUR

●

●

Assumption: per yearequipped for individual billing

Calculation– Transponders 1 mill. Bins x 5 EUR =

5 mill. EUR

– Truck installation100 trucks x 30,000 EUR =3 mill. EUR

Total: 8 mill. EUR➱

Individual billing systems: Costs Market volume for individualbilling systems

MSW collection in EuropeExisting bins: 113 mill. units (2002)

Individual billing systems10 mill. €

9 %

● Major market is Germany withindividual billing systems forapprox. 6 mill. bins

Figure 5.16. Market penetration and market volume.

5.2.5 Deposit automats for bottles/cans

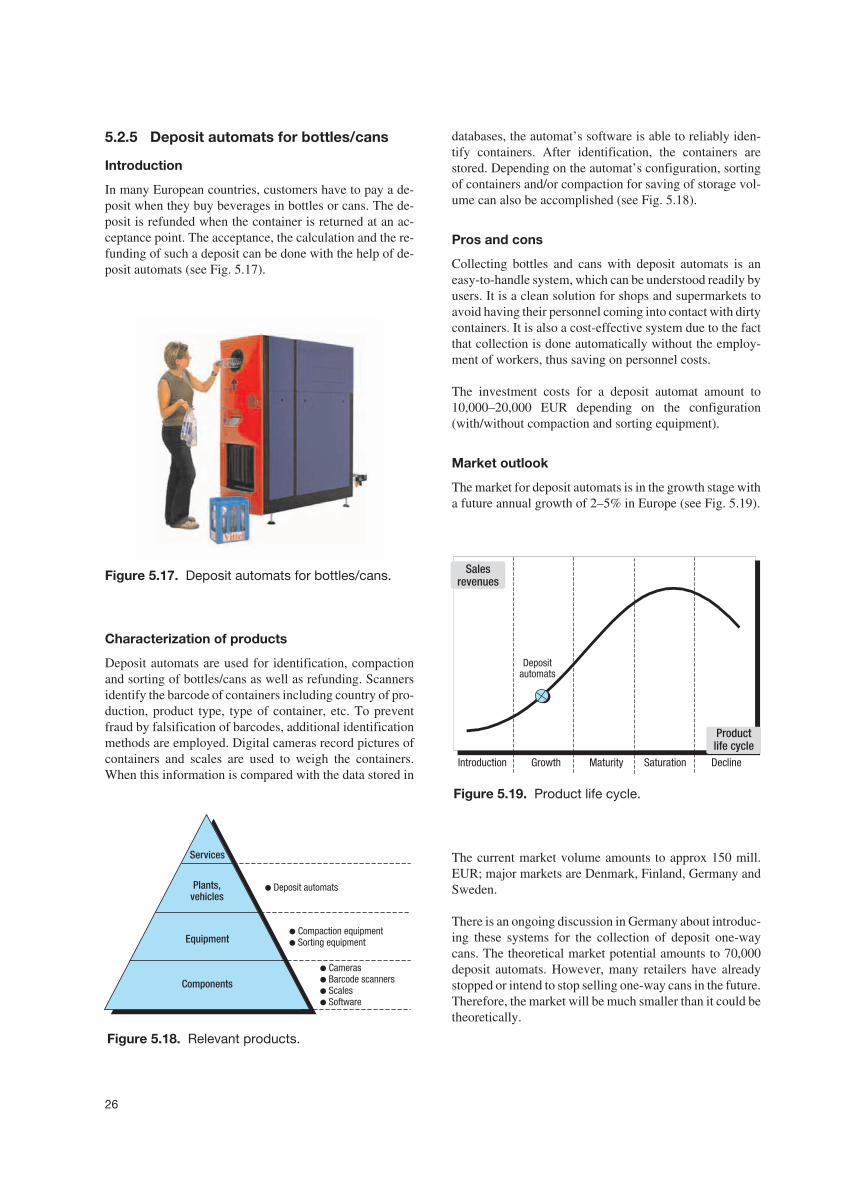

Introduction

In many European countries, customers have to pay a de-posit when they buy beverages in bottles or cans. The de-posit is refunded when the container is returned at an ac-ceptance point. The acceptance, the calculation and the re-funding of such a deposit can be done with the help of de-posit automats (see Fig. 5.17).

Characterization of products

Deposit automats are used for identification, compactionand sorting of bottles/cans as well as refunding. Scannersidentify the barcode of containers including country of pro-duction, product type, type of container, etc. To preventfraud by falsification of barcodes, additional identificationmethods are employed. Digital cameras record pictures ofcontainers and scales are used to weigh the containers.When this information is compared with the data stored in

databases, the automat’s software is able to reliably iden-tify containers. After identification, the containers arestored. Depending on the automat’s configuration, sortingof containers and/or compaction for saving of storage vol-ume can also be accomplished (see Fig. 5.18).

Pros and cons

Collecting bottles and cans with deposit automats is aneasy-to-handle system, which can be understood readily byusers. It is a clean solution for shops and supermarkets toavoid having their personnel coming into contact with dirtycontainers. It is also a cost-effective system due to the factthat collection is done automatically without the employ-ment of workers, thus saving on personnel costs.

The investment costs for a deposit automat amount to10,000–20,000 EUR depending on the configuration(with/without compaction and sorting equipment).

Market outlook

The market for deposit automats is in the growth stage witha future annual growth of 2–5% in Europe (see Fig. 5.19).

The current market volume amounts to approx 150 mill.EUR; major markets are Denmark, Finland, Germany andSweden.

There is an ongoing discussion in Germany about introduc-ing these systems for the collection of deposit one-waycans. The theoretical market potential amounts to 70,000deposit automats. However, many retailers have alreadystopped or intend to stop selling one-way cans in the future.Therefore, the market will be much smaller than it could betheoretically.

26

Figure 5.17. Deposit automats for bottles/cans.

Equipment

Services

Plants,vehicles

Components

●

● Sorting equipmentCompaction equipment

● Deposit automats

●

●

●

●

Barcode scannersScalesSoftware

Cameras

Figure 5.18. Relevant products.

Introduction Growth Maturity Saturation Decline

Depositautomats

Salesrevenues

Productlife cycle

Figure 5.19. Product life cycle.

Competition

The market for deposit automats in Europe is dominated bythe Norwegian company Tomra, which has a market shareof more than 50%. Further suppliers exist, however, with asmall market share.

Conclusion

The market for deposit automats is very attractive due tothe large volume of approx. 150 mill. EUR and the mediumgrowth rate. There are only a few suppliers, therefore thecompetitive pressure is not very intensive.

5.2.6 Suction system

Introduction

Traditionally, MSW is collected in waste bins by citizens.These waste bins are placed near houses or apartments,generally in special waste bin rooms or other specifiedplaces. Waste collection trucks collect and empty thesebins at regular intervals. This system for collection of mu-nicipal solid waste has some disadvantages. The waste col-lection process is associated with noise and odour. Incrowded or remote areas collection trucks also have prob-lems reaching the bins. These and other factors led to thedevelopment of suction systems for the collection and stor-age of MSW.

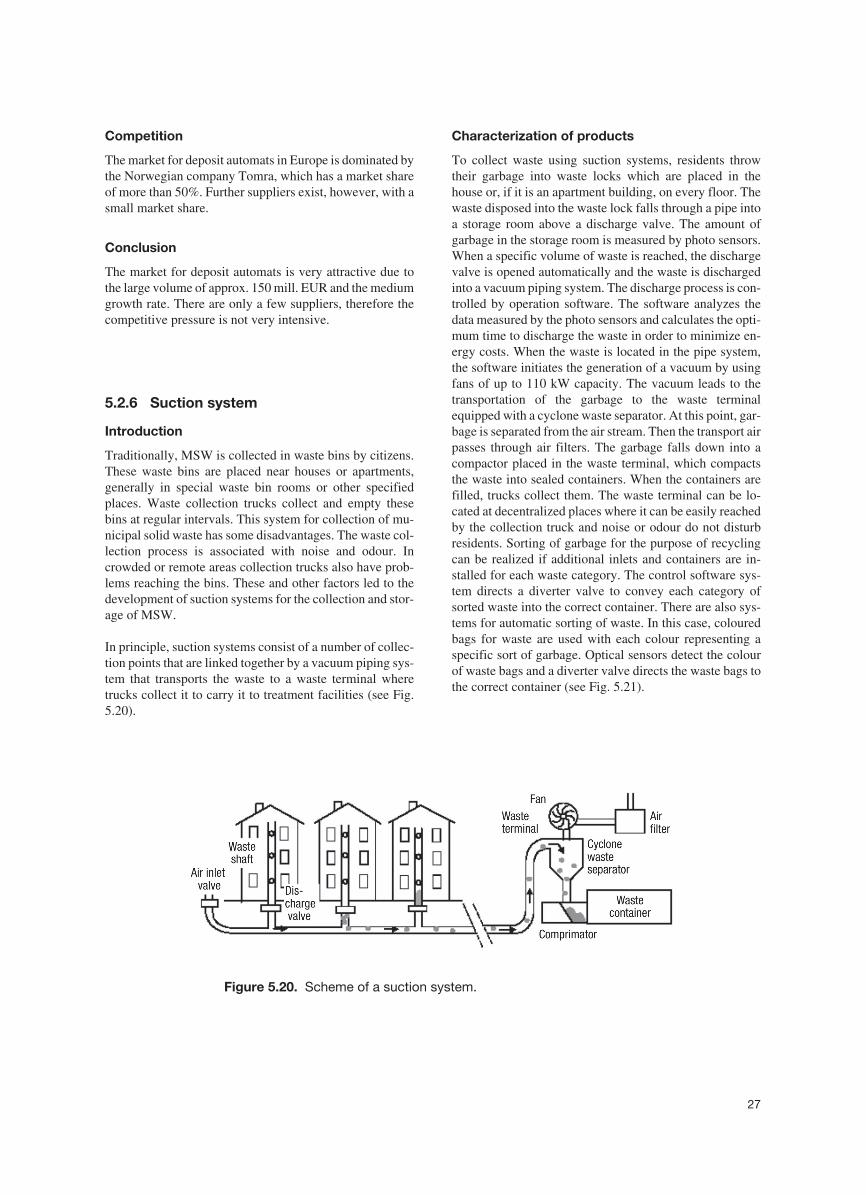

In principle, suction systems consist of a number of collec-tion points that are linked together by a vacuum piping sys-tem that transports the waste to a waste terminal wheretrucks collect it to carry it to treatment facilities (see Fig.5.20).

Characterization of products